The Bureau of Labor Statistics (BLS)

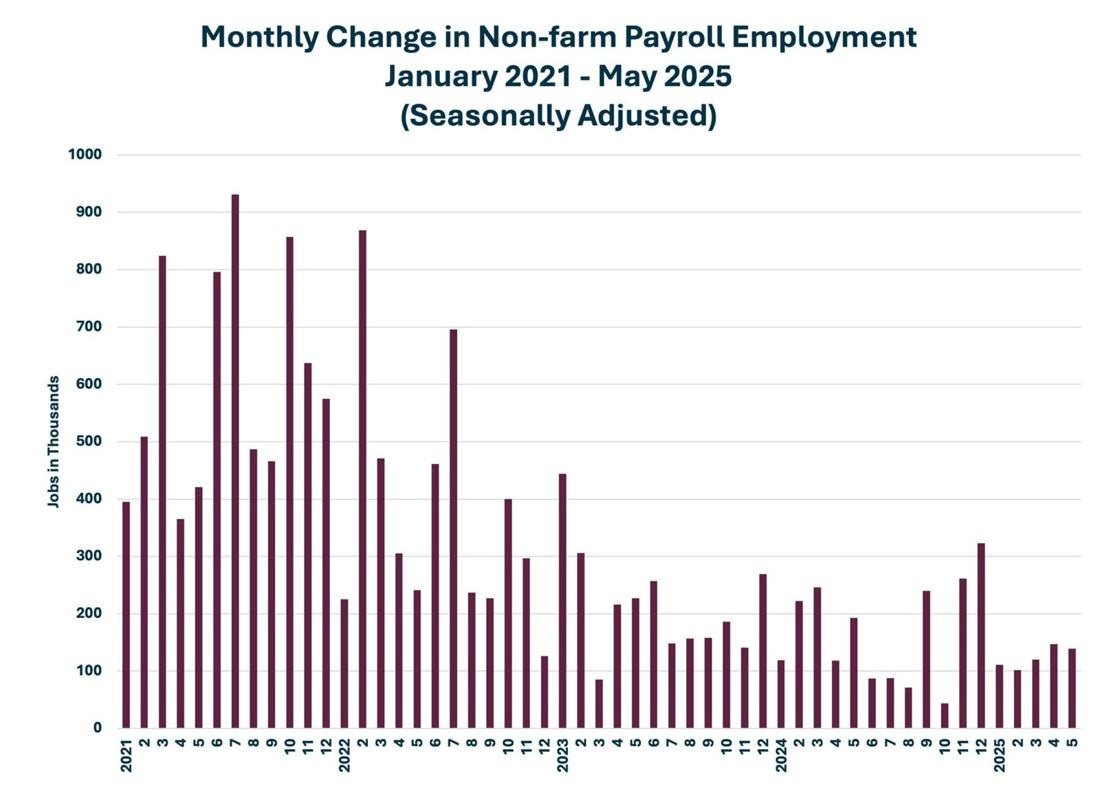

reported this morning that total non-farm employment increased by 139,000 in May, and the unemployment rate remained steady at 4.2 percent.

Some analysts thought that today’s report would give some indication of the economy’s direction:

is growth subsiding or speeding up?

While there are indications of economic sluggishness, a fair reading of today’s jobs report would suggest a labor market treading water. A broader view that includes other recent labor market statistics, however, justifies greater vigilance and caution.

Why greater vigilance?

Despite a normal looking jobs report, there are some indicators of a slowdown.

The labor force participation rate declined from 62.6 to 62.4 percent.

This statistic measures the percent of the civilian population (which is non-institutionalized population 16 years old and above) that is employed or looking for work.

This important statistic had changed little over the year.

A similar decrease occurred in the employment population ratio: a decline from 60.0 to 59.7 percent.

This statistic measures the percentage of the civilian population that is employed.

Both metrics registered statistically significant decreases.

Also declining significantly was the total number of people employed.

This measure dropped by 695,000.

Total employment now stands at an estimated 163,273,000.

Also declining were BLS estimates for total employment in March and April.

BLS reduced its March estimate by 65,000 and its April estimate by 30,000.

Some will read that total downward revision as further evidence of economic slowing, even though it may just be the inclusion of more sample by the Bureau.

BLS allows firms to submit their surveys responses for two months following the initial release date.

Figure 1

The decline in total employment is almost entirely explained by a statistically significant increase in the number of people leaving the labor force, presumably because of retirement. It is important to remember that if a person leaves a job but is looking for work, they remain in the labor force. The number not in the labor force increased in May by 813,000 and now stands at 102,875,000. The total number of people unemployed only increased by 71,000 and now stands at 7,237,000.

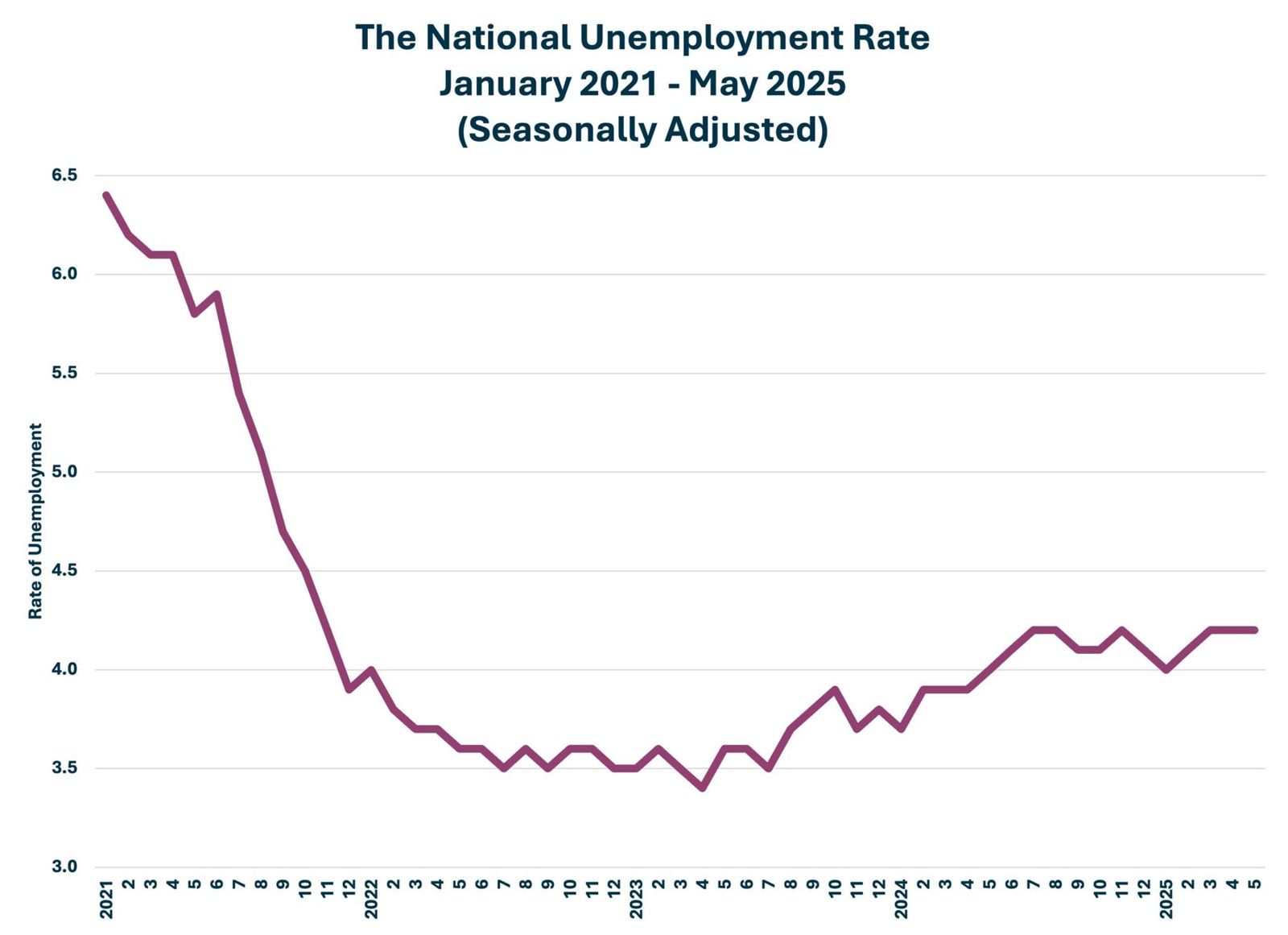

Figure 2

None of the unemployment rates for the principal race and ethnicity groupings changed significantly, and there was very little movement in unemployment rates by educational attainment.

However, this may change.

An important but seldom noted statistic in the monthly jobs report has been recently trending down steadily – the total private diffusion index. This metric measures the percent of private sector employers that are adding jobs.

A reading of more than 50 percent shows job expansion.

The statistic stood at 52.6 a year ago and 51.8 in April.

The May estimate is 50.0.

A similar diffusion index for manufacturing is already below 50 percent and now stands at 41.7 percent.

Considerable attention has been paid to the President Trump’s effort to reduce the number of federal employees.

This month’s jobs report shows that the unemployment rate for all government workers, including state and local, increased from 1.8 to 2.0 percent, and that increase is attributable to federal employment.

Total federal employment (excluding the U.S. Postal Service) declined by 22,000 in May.

Total

federal government employment now is 42,000 lower than a year ago, on a seasonally adjusted basis.

Further evidence of possible economic slowing appeared in a BLS report released on June 5:

Productivity and Costs for the First Quarter of 2025. BLS produces quarterly estimates of non-farm labor productivity, which basically measures the seasonally adjusted average output per worker.

The revised first quarter 2025 estimate was a negative 1.5 percent change over the fourth quarter of 2024.

That is the first quarterly decrease since the second quarter of 2022. The quarterly declined stemmed from a decrease in output (-0.2 percent) and an increase in hours worked (1.3 percent).

The Demand for Labor Falls

Another metric to watch as we try to determine the direction of the economy is the demand for labor.

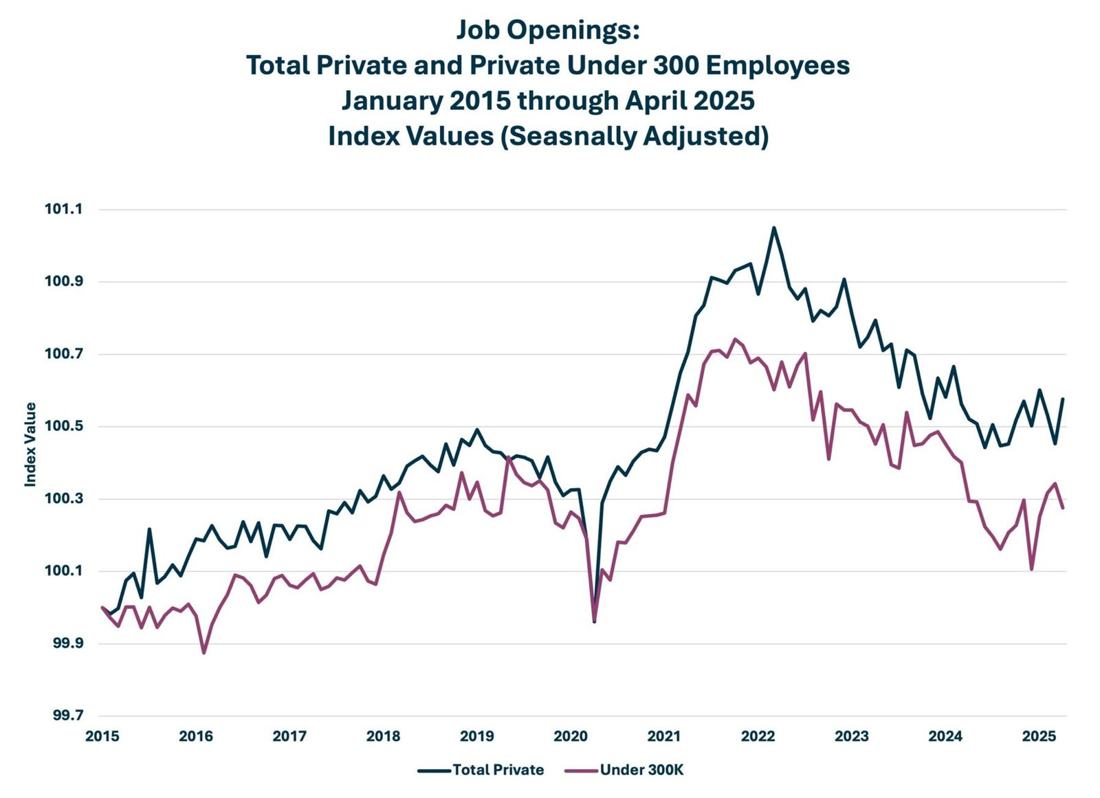

One of the curious features of the current economy is the uncertain direction of job openings that began in March of 2022.

Is the long decline continuing or has the economy found a plateau for labor demand, post the inflation of 2022 through 2024?

According to the latest Job Openings and Labor Turnover report from BLS,

total private openings have fallen from 11.1 million in March of 2022 to 6.5 million in April of 2025, or a total decline of 4.6 million openings.

That said, there’s been little net change over the past several months.

Figures 1 and 2 show this slackening in labor demand.

Figure 3 compares the total private jobs openings to openings in small to medium-sized firms, or companies with 100 to 300 employees.

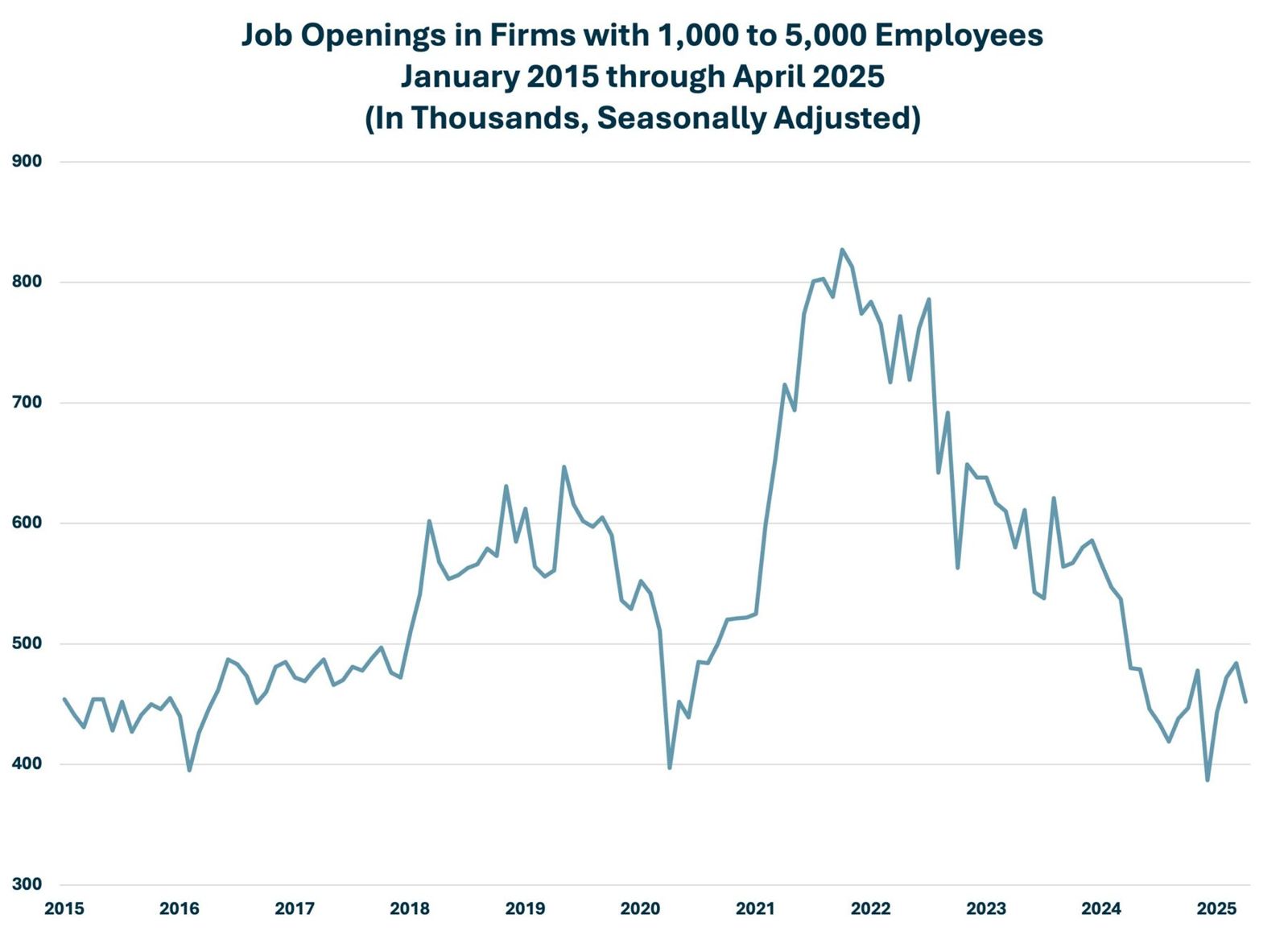

Figure 4 shows a similar decline among firms with 1,000 to 5,000 employees.

Figure 3

Figure 4

Of course, economists expect high labor demand following a serious slowdown or recession, as we experienced in 2020 and early 2021.

The U.S. economy certainly experienced that burst in demand.

However, economists also expect the resumption of economic growth to include a steady upward rise in labor demand, as we can see above from 2015 through 2019.

Statistically and visually, labor demand appears to be treading water.

Much depends on whether that drop in labor productivity signals a slowdown or the possibility of more inflation assures more sluggish growth.

Thus, it is more important to watch the demand side of labor markets in the near term than the supply side.

Price Changes Favored Working Households in April

While labor markets signaled a possible slowdown, working households had to feel a little better when assessing their growing purchasing power.

The Bureau of Labor Statistics (BLS) issued three important price indexes in May, and market leaders and policy makers eagerly anticipated each one.

Why, one might ask?

Many analysts thought that the May price reports would give us the first significant indication of how much price change the administration’s tariff policies would produce.

It is fair to say that price watchers expected tariffs to raise prices and restart inflation. Household purchasing power hinges in part on the direction and volatility of price changes.

Assuming that the administration succeeds in overturning a recent court ruling gutting against their trade policy, tariffs may still do that.

However, everyone will need to wait for another month’s round of index reports.

BLS’s May reports were decidedly mixed.

The closely watched Consumer Price Index (CPI) rose by 0.2 of a percent from its March level (which fell by 0.1 percent from February), and the CPI rose by 2.3 percent on an annual rate.

That increase might indicate a tariff effect, but analysts will need to see more data before drawing that conclusion.

The second index, the Producer Price Index (PPI), which follows non-labor production inputs, decreased by 0.5 percent in April after being unchanged in March.

That decrease produced contrary evidence of a tariff effect.

The PPI grew by 2.4 percent on an annual rate, or from April 2024 through April 2025.

Thus, it comes down to the Import and Export Price Indexes.

The import prices should be most affected by the administration’s tariffs and the Import Price Index did increase by 0.1 percent in April after falling by 0.4 percent in March.

However, import prices are now growing at a paltry annual rate of 0.1 percent, which is hardly a signal that tariffs are raising prices.

The Export Price Index rose by 0.1 percent and now shows an annual rate of 2.0 percent.

So, is there no evidence to affirm the claim that tariffs will raise prices?

Perhaps.

On the one hand, an enormous 12 percent drop in the April import prices for fuels completely overshadowed price increases in many other parts of the overall index.

If the fuel prices are excluded, then the monthly change in the Import Price Index rises to 0.4 percent and the annual rate grows to 1.2 percent.

On the other hand, the prices for commodities that should most be affected by tariffs (like apparel, shoes, and automobiles) hardly changed month-over-month.

In fact, shoe imports dropped in price, even though 63 percent of shoe imports come from two countries heavily affected by tariffs: China and Vietnam.

It is altogether possible that April prices reflected the apparently dramatic buildup in inventories that occurred in March as importers anticipated higher tariffs and, perhaps, some margin reduction as retailers attempt to defend market share by cutting profits.

In short, the jury is still out on how much and when tariffs will cause overall price increases.

That said, households won the purchasing power battle in April, when average wages rose at a faster rate than the CPI.

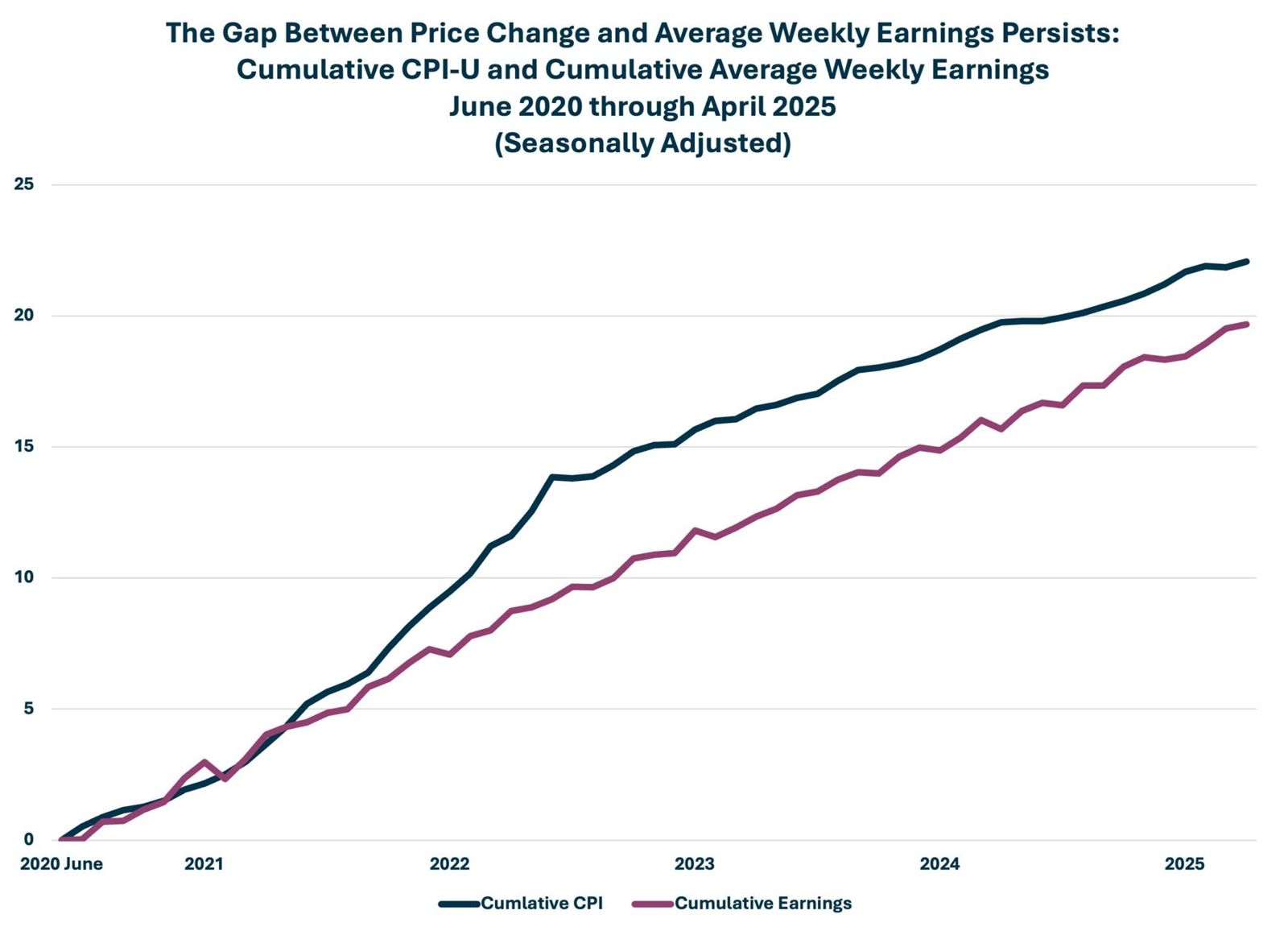

As Figure 5 shows, households are still clawing back purchasing power that they lost during the serious inflation period that began in June of 2021.

Figure 5

Average weekly earnings for all private employees grew at an annual nominal rate of 4.1 percent, while the CPI rose at an annual rate of 2.3 percent.

The purchasing power gap has closed by 55 percent since its peak in June of 2022.

Conclusion

In isolation, this monthly employment report should raise few concerns.

Employment gains are near their monthly average of the past year, and the unemployment rate is unchanged.

However, the context is all important.

Surrounding the monthly numbers are downward revisions, worrisome productivity changes, slowing demand for labor, and sliding participation rates.

Yes, treading water may be a good way to view this month’s statistics, but, given the larger context,

there is every reason to remain watchful and cautious about the current trend of economic activity.