Testimony

Remarks before Congress by Dr. Bill Beach on "Reducing America’s National Debt: Rooting Out Federal Waste, Fraud, and Overregulation"

May 14, 2026 · William W. Beach, D. Phil.

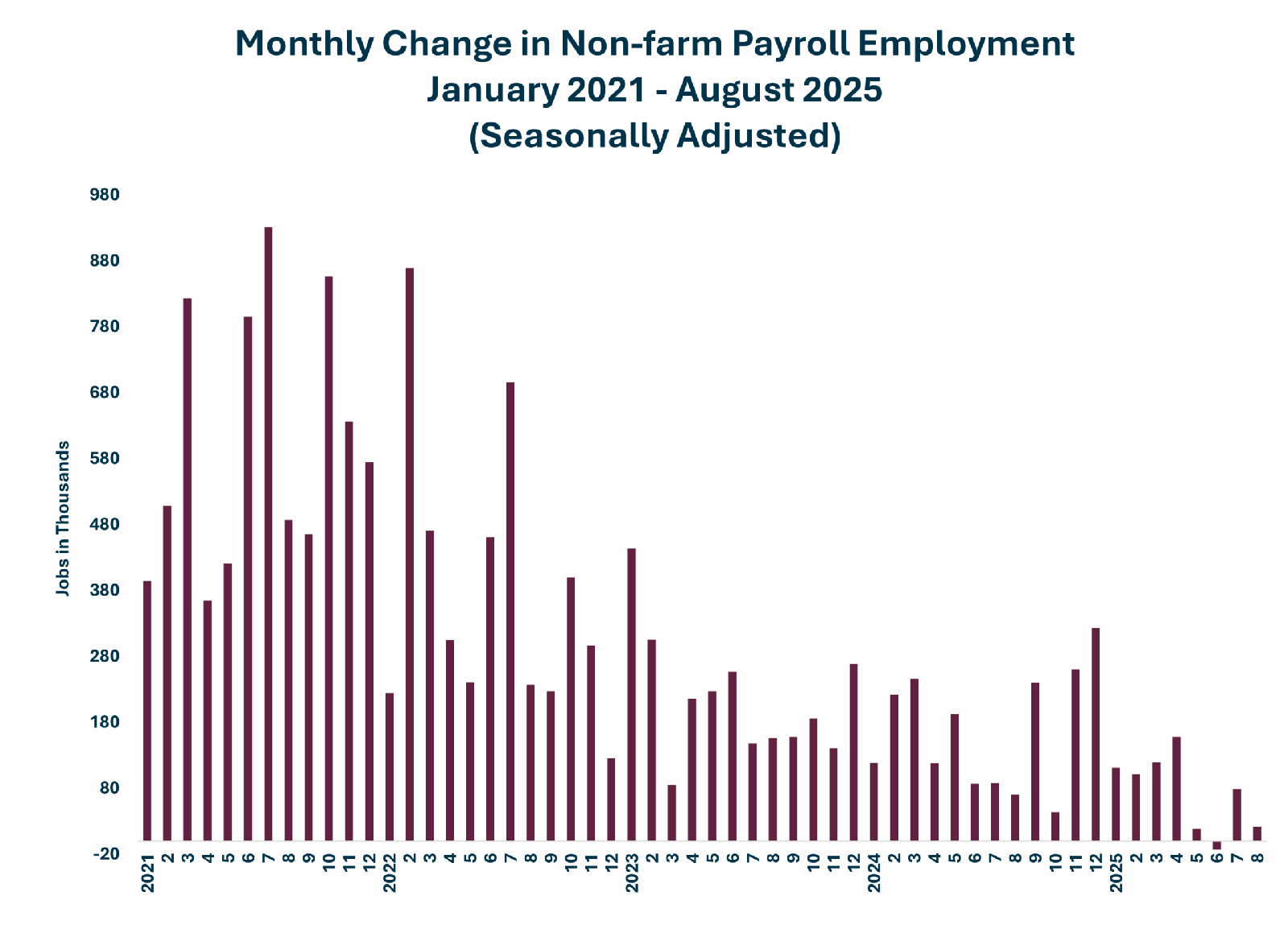

The private sector grew by 38,000 net new jobs in August, which was partially offset by a contraction in government of 16,000 jobs. Behind this increase in private sector employment, however, stands a sharp drop in the goods producing sector. That sector declined by 25,000 jobs. Leading that decline was durable manufacturing, which shed 19,000. Indeed, all other goods producing sectors (i.e., construction, mining, logging) showed declines except non-durable manufacturing, which grew by 7,000 jobs.

The sector gains this month all stemmed from the service sector, which grew by 63,000. The biggest gainer this month, as it was last month, was in health care, which grew by 46,800 jobs. However, several service sectors showed declines in jobs: wholesale trade dropped by 11,700, and professional and business services declined by 17,000.

An additional source of slow growth in August was the government sector. Overall, this sector shed 16,000 jobs, with federal employment leading the way: federal government employment dropped by 15,000. However, state government employment also declined by 13,000. These declines were partially offset by a 12,000 gain in local employment, mostly in education.

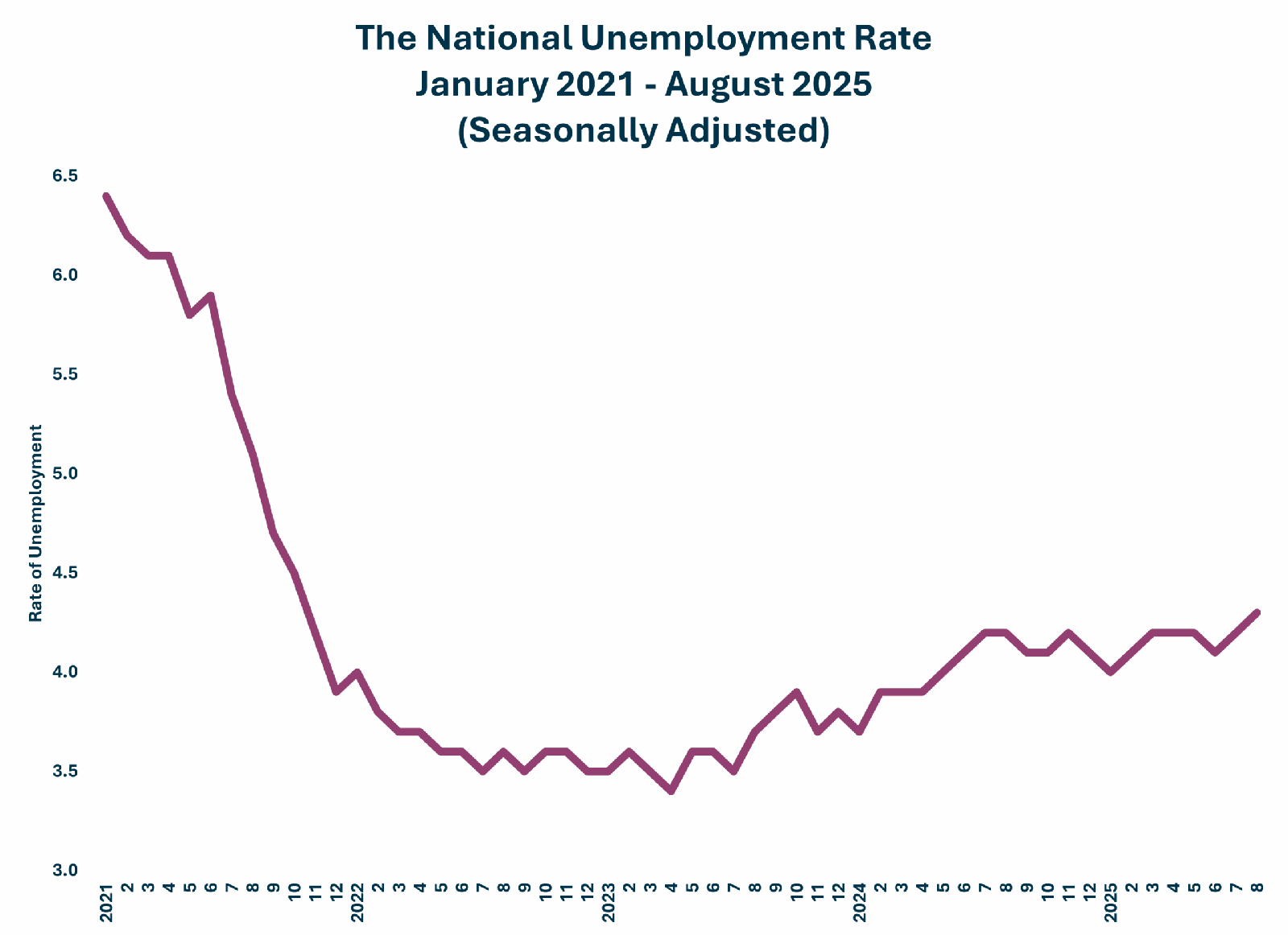

Today’s Employment Situation report also contained labor force estimates from the household survey. It is this survey (formerly known as the Current Population Survey) that yields the unemployment rates, labor force participation rates, and other demographic characteristics of American workers. BLS reported a slight increase in the overall unemployment rate from a seasonally adjusted 4.2 to 4.3 percent. Very small increases occurred in all the demographic groups, except teenagers, where the unemployment rate declined by 1.3 percentage points to 13.9 percent, and Asian workers, where the rate dropped by 0.3 percent points to 3.6 percent.

The private sector grew by 38,000 net new jobs in August, which was partially offset by a contraction in government of 16,000 jobs. Behind this increase in private sector employment, however, stands a sharp drop in the goods producing sector. That sector declined by 25,000 jobs. Leading that decline was durable manufacturing, which shed 19,000. Indeed, all other goods producing sectors (i.e., construction, mining, logging) showed declines except non-durable manufacturing, which grew by 7,000 jobs.

The sector gains this month all stemmed from the service sector, which grew by 63,000. The biggest gainer this month, as it was last month, was in health care, which grew by 46,800 jobs. However, several service sectors showed declines in jobs: wholesale trade dropped by 11,700, and professional and business services declined by 17,000.

An additional source of slow growth in August was the government sector. Overall, this sector shed 16,000 jobs, with federal employment leading the way: federal government employment dropped by 15,000. However, state government employment also declined by 13,000. These declines were partially offset by a 12,000 gain in local employment, mostly in education.

Today’s Employment Situation report also contained labor force estimates from the household survey. It is this survey (formerly known as the Current Population Survey) that yields the unemployment rates, labor force participation rates, and other demographic characteristics of American workers. BLS reported a slight increase in the overall unemployment rate from a seasonally adjusted 4.2 to 4.3 percent. Very small increases occurred in all the demographic groups, except teenagers, where the unemployment rate declined by 1.3 percentage points to 13.9 percent, and Asian workers, where the rate dropped by 0.3 percent points to 3.6 percent.

One statistic in the household survey did move in a statistically significant direction. That was new entrants to the labor force. This indicator dropped by 199,000 from July. This result may well reflect the administration’s successful effort to reduce the number of immigrants entering the U.S. labor force. That said, the aggregate estimate of 786,000 new entrants in August is in line with its year-ago level of 708,000.

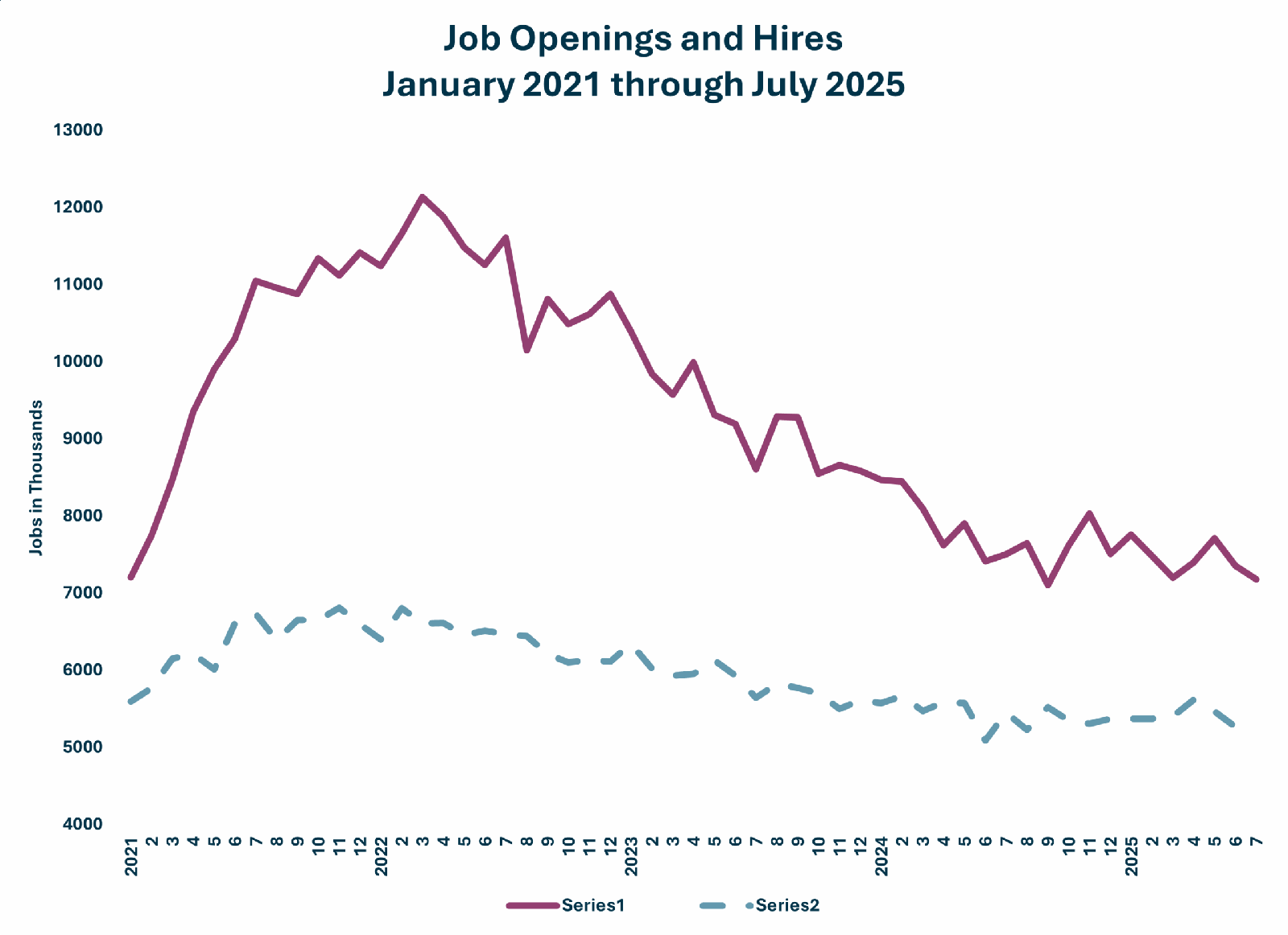

Market analysts broadly expected the August estimate to show more slowing in total employment change. The BLS release on Wednesday of the latest Job Openings and Labor Turnover Survey (JOLTS) reinforced that view. This important, market-moving report estimates the demand for labor rather than supply changes, which the monthly Employment Situation report describes. This month’s JOLTS covered the July reporting period and showed a slight decline in the principal demand categories: job openings and hires. That slight change in demand is consistent with the overall picture on the supply side of summer declines in job growth, even though the current estimate for July shows a 79,000 increase. Openings are down by 323,000 from a year ago, and hires have declined by 143,000.

One statistic in the household survey did move in a statistically significant direction. That was new entrants to the labor force. This indicator dropped by 199,000 from July. This result may well reflect the administration’s successful effort to reduce the number of immigrants entering the U.S. labor force. That said, the aggregate estimate of 786,000 new entrants in August is in line with its year-ago level of 708,000.

Market analysts broadly expected the August estimate to show more slowing in total employment change. The BLS release on Wednesday of the latest Job Openings and Labor Turnover Survey (JOLTS) reinforced that view. This important, market-moving report estimates the demand for labor rather than supply changes, which the monthly Employment Situation report describes. This month’s JOLTS covered the July reporting period and showed a slight decline in the principal demand categories: job openings and hires. That slight change in demand is consistent with the overall picture on the supply side of summer declines in job growth, even though the current estimate for July shows a 79,000 increase. Openings are down by 323,000 from a year ago, and hires have declined by 143,000.

Today’s jobs report may be highly consequential. The estimates from May through August will reinforce the Federal Reserve’s concerns about the health of U.S. labor markets. Thus, today’s report puts pressure on the Fed to make moves on the Fed Funds Rate. Likewise, analysts will be pouring over the report to see if the sharp change in tariff policies inaugurated last spring are putting downward pressure on employment growth. That appears to be in the case in the goods sectors and may explain some of the current declines in service-providing sectors like professional business services. However, more digging into the labor and price data are needed to draw any clear conclusions.

Today’s jobs report may be highly consequential. The estimates from May through August will reinforce the Federal Reserve’s concerns about the health of U.S. labor markets. Thus, today’s report puts pressure on the Fed to make moves on the Fed Funds Rate. Likewise, analysts will be pouring over the report to see if the sharp change in tariff policies inaugurated last spring are putting downward pressure on employment growth. That appears to be in the case in the goods sectors and may explain some of the current declines in service-providing sectors like professional business services. However, more digging into the labor and price data are needed to draw any clear conclusions.