The Bureau of Labor Statistics (BLS)

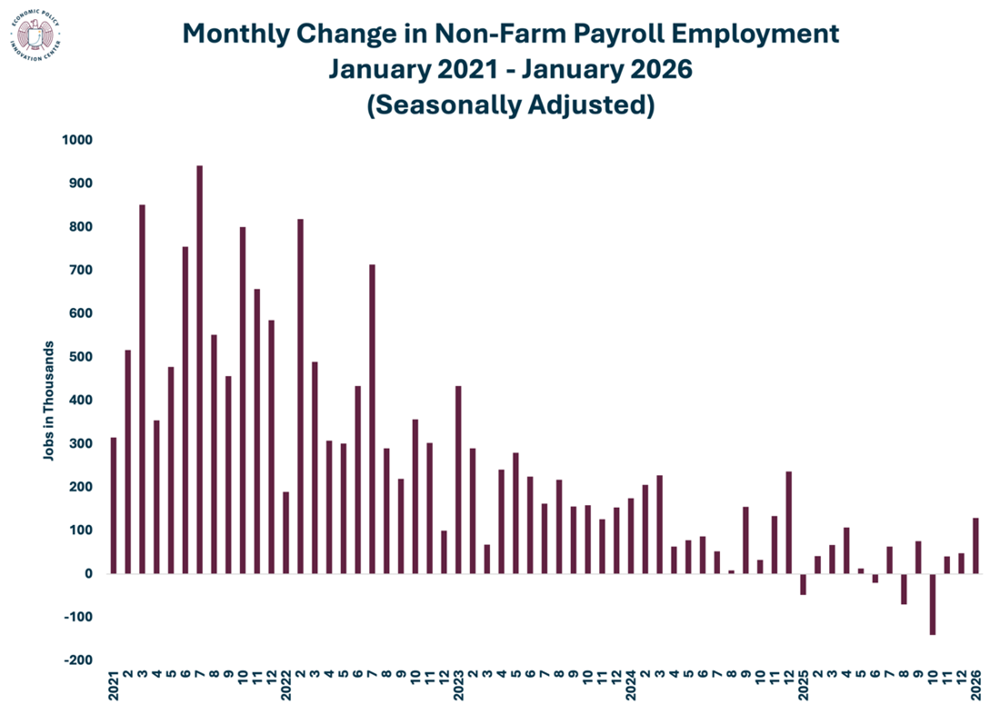

released one of its most complex labor market reports in over a year. The national media will focus on the unexpectedly high job gain of 130,000 (well above the consensus forecast of 55,000) and the slight dip in the unemployment rate from 4.4 to 4.3 percent. Others will note the strengthening in manufacturing and construction employment, which had been faltering over the past year. BLS tempered this good news with small but telling reductions in the jobs estimates for November and December, reducing November by 15,000 to a final estimate of 41,000 jobs gained, and December from 50,000 to 48,000 for that month’s first revision.

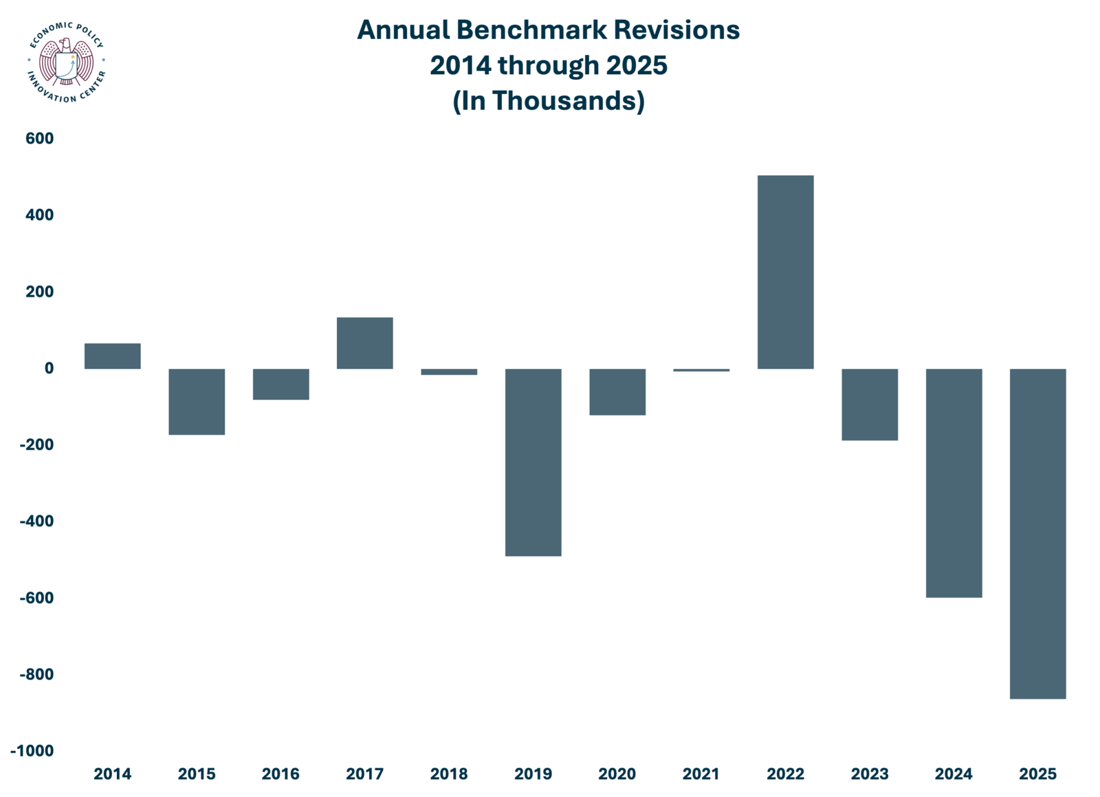

The big news, however, was the dramatic downward revision in total non-farm employment stemming from the annual benchmark exercise.

[1] Let’s begin unwinding this complex report with a dive into the annual benchmark.

Revisions to the Jobs Data

BLS used the March 2025 count of all jobs as reported in the Quarterly Census of Employment and Wages (QCEW) to determine how much BLS had missed the actual number of jobs in the economy when it made its survey-based estimate for that month. The Bureau found that its survey-based estimate of 159,275,000 non-farm jobs was too high by a seasonally adjusted 898,000.

[2] The actual count based on the QCEW was 158,377,000.

Because of this benchmark, BLS revised downward total employment for each month in 2025. For all of 2025, BLS reduced net job growth from 585,000 to 181,000.

The chart above shows the magnitude of this revision over the period 2014 through 2025. Though not the biggest change ever in its recent benchmarking history (that honor goes to the March 2009 benchmark of 902,000), it will underscore concerns that something is amiss in BLS’s monthly effort to estimate total jobs. The Bureau is engaged in intensive efforts to improve its estimation techniques, and we hope that those efforts focus on three potential candidates for estimation error.

- First, BLS uses a model that estimates job changes stemming from firms that come into existence during the year and create jobs and those that disappear or die. This “birth/death model” is likely the source of some of the monthly estimating error.

- A second candidate is BLS’s reliance on historical labor force estimates that overshot the number of immigrant workers. The Census Bureau has dramatically reduced its immigrant population estimates for 2024 and 2025 but only after BLS began using Census estimates in its estimates of labor force growth. These lower immigrant counts reflect policy changes on immigration made by the Biden Administration in 2024 and the Trump Administration throughout 2025.

- Finally, there is a possibility that the QCEW might itself be a source of error. BLS spends a great deal of time and resources making the March quarterly QCEW results as good as possible. Remember that the states supply the data for the QCEW from their own unemployment insurance records. Unfortunately, the performance of the states in doing this is very uneven, which is why BLS spends so much time making certain that the March quarter, that important benchmark quarter, is as good as it can be. The other three quarters, however, likely suffer from less accurate state contributions. Thus, when BLS uses the other quarters during the year to audit its birth/death model during, it may be getting less reliable indications of job market changes.

January Data Encourages Cautious Optimism

Now, back to January’s labor market metrics. The headline numbers (

130,000 net new jobs in January and a 4.3 percent unemployment rate) also contain some important information. Let us first start with the change in total non-farm employment.

The private side of the economy in January produced a stunning 172,000 estimated new jobs. This is well above the rate of job creation needed to keep the unemployment rate steady, which is likely sitting around 70,000. Job gains were widespread, particularly in health care (123,500), construction (33,000), professional and business services (34,000), and durable manufacturing (9,000). This last entry on the plus side is particularly noteworthy, given manufacturing employment declines in 2025.

Sectors losing jobs included government (-42,000, of which federal government employment declined by 34,000), financial services (-22,000), and information (-12,000). Despite these losses, the private sector has been consistently positive in 2025. Prior to the January numbers being announced, the three-month moving average of job growth had been consistently in the 50,000 range. January’s unexpectedly high growth increased the three-month average to 103,000.

It likely is too early to claim a new trend from that of soft job growth, which analysts have seen over the past year. That said, some additional support for seeing labor market improvement comes from the survey of households reported in this month’s Employment Situation Report.

Unemployment Drops, But Not Significantly

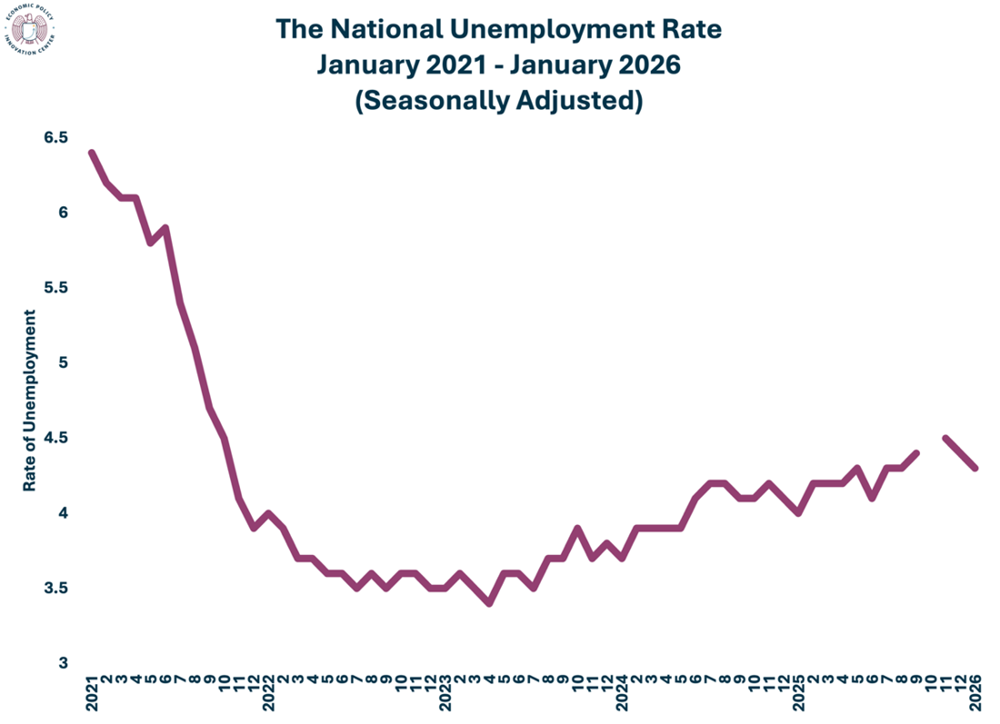

As noted, the unemployment rate slipped down from 4.4 to 4.3 percent. This is the third consecutive decline, though the rate remains elevated from its 4.0 rate in January 2025. This small, barely significant decline was accompanied by a stronger signal from the number of people unemployed for 27 weeks or more: that estimate dropped by 113,000. The population of long-term unemployed now stands at 1,835,000. More broadly, the total number of unemployed dropped by 141,000, which brought the population of unemployed to 7,362,000.

Perhaps another sign of greater labor market vitality is the change in those working part-time because they cannot find full-time work. That population dropped by a statistically significant -453,000. A companion measure, working part-time for non-economic reasons, rose: 566,000 more workers fit into this category, and growth here is often interpreted as a positive labor market signal.

Other labor force metrics from the Household Survey weakly flashed greater labor market health. The labor force participation rate (which measures the percentage of the civilian population aged 16 and above that is working or looking for work) rose 0.1 of a percent to 62.5 percent. Likewise, the employment population ratio (the percentage of the civilian population that is working) rose 0.1 of a percent to 59.8 percent. Nearly all of the basic metrics showed no statistically significant change from last month, and that can be viewed as good news.

BLS’s reading for the January jobs market leaves analysts wondering whether the sluggish times of 2025 are indeed over. The benchmark revision could be the final stanza of last year’s jobs dirge, but, as always, we need to wait for more data.

[1] BLS performs this benchmarking estimated every year. The Bureau announces a preliminary estimate in August followed by a final estimate of error in February. This year the preliminary estimate came in at a reduction in total non-farm employment of 919,000 (not seasonally adjusted).

[2] BLS first revises all the estimates from April 2024 through December 2025 on a not-seasonally adjusted basis, again based on the benchmark month of March 2025. The not-seasonally adjusted March 2025 miss was -862,000. BLS then applies seasonal factors to the monthly unadjusted numbers to produce the seasonally adjusted estimates for 2025. BLS reported these monthly estimates in the February Employment Situation Report.