Our country is nearing its 250th anniversary, and America’s most injurious vice is coming to the fore of our political discourse. The

national debt has become a drain on our economy, and rather than addressing the problem, we have punted real solutions in favor of resolving debt with more debt. Our Founding Fathers, too, dealt with the issue of public debt, and their solutions for fiscal and monetary policymaking deserve revisiting.

In the decade that followed U.S. independence, the Continental Congress struggled to repay the high interest-bearing debt accrued during the Revolutionary War. The Articles of Confederation outlined no means for Congress to generate revenue, and as a result, the federal government rolled over much of the interest on its wartime debt by financing payments to creditors with new debt.

While the Constitution’s provisions remedied this problem in 1789 by giving Congress the ability to create tax revenue, the federal government faces an eerily similar, yet immensely larger problem today. To explain the severity of our current fiscal position compared to that of the 1780s: post-Revolutionary War public debt amounted to roughly 40% of early U.S. GDP, while our national debt today weighs in at approximately 121% of total U.S. GDP. In 2025 alone, $9.3 trillion of public debt is set to mature, nearly $3 trillion of which the federal government has already rolled over by issuing more debt. The government is expected to run a deficit of $2 trillion, meaning that the United States Treasury will have to borrow more than

$11 trillion to finance our existing debt and new deficit.

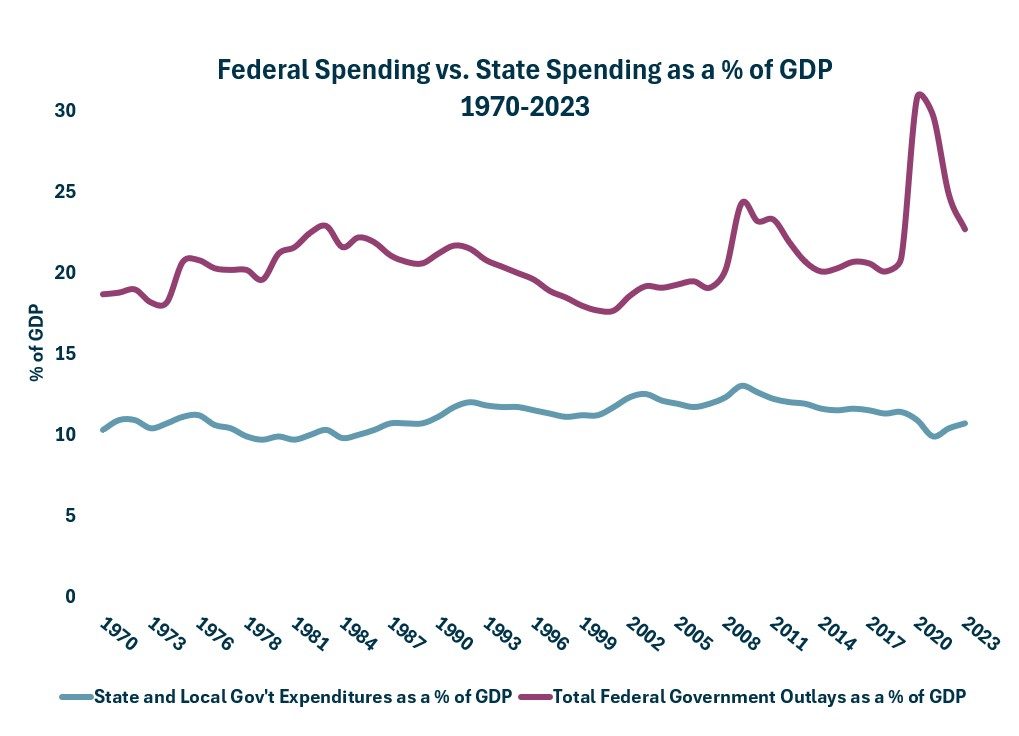

As U.S. bond markets teeter, interest rates climb, and investors begin considering options beyond the United States, we must ask how we as a country have placed ourselves in a worse financial position than we were in at the time of our nation’s founding. We know that spending has skyrocketed. For example, total federal outlays rose from $3.5 trillion in 2014 to more than $6.4 trillion in 2024, an increase of over 80% in just ten years. But what specific fiscal habits have driven this?

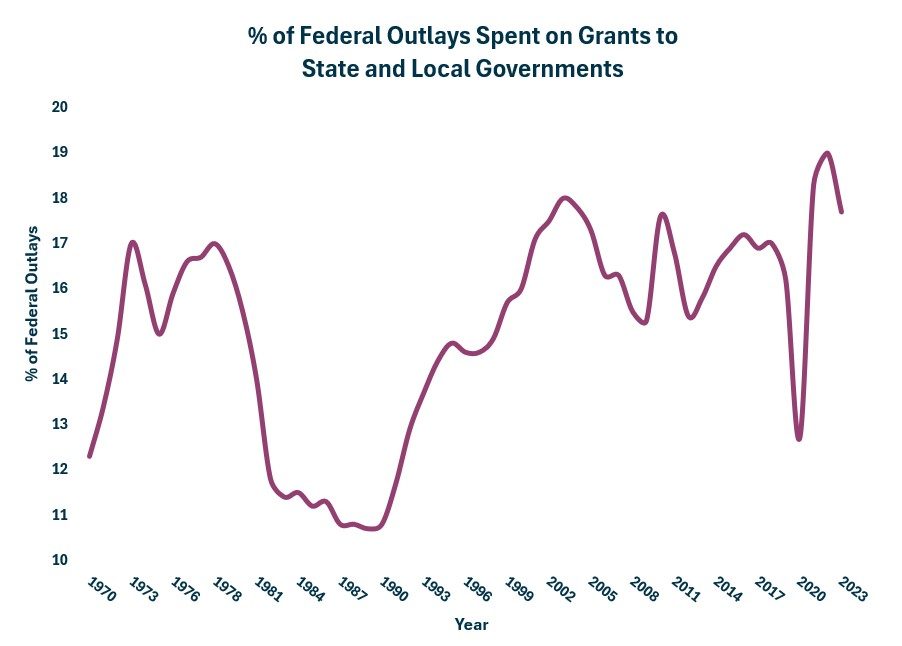

One key change in government financing in the past 20 years is the gradual centralization of program funding. The federal government has begun financing programs for states at an extremely steep price for taxpayers. According to Treasury data, federal grants to states rose from $500 billion in 2004 to more than $1.3 trillion in 2024, an increase of 160%. Not only does this centralize power in the federal government, but it requires the federal government to take on more and more financial risk to fund these state-led programs. States are incentivized to expand these programs to increase their federal funding, which they in turn use to replace their own state revenue.

While the national debt has exponentially increased since the turn of the century, debt held by state governments has markedly decreased. Treasury data show that state government debt fell from about $1.3 trillion in 2010 to $970 billion in 2023, even as federal debt surged by more than

$20 trillion during the same period. And though the federal government has not seen revenue growth adequate to offset its rapidly increasing spending, state governments have consistently seen revenue growth and frequently operate at surpluses; In fact, a 2023 Census Bureau report showed 45 states ended the fiscal year in surplus.

This phenomenon is in no one’s best interest. It disincentivizes states from cutting down on waste, fraud, and abuse in the programs they lead. As the federal government is paying for these programs, states have no reason to administer them as efficiently as possible.

For instance, the federal government reported $543 billion in improper payments in Medicaid alone over the past ten years, driven by insufficient state oversight and eligibility errors. But that was based on only partial measurements; a joint EPIC and Paragon analysis pegged Medicaid’s improper payments at $1.1 trillion

. And while it may save states from sharing the burden of their welfare costs, it ultimately hurts all citizens and taxpayers by jeopardizing our country’s ability to borrow in the future and the dollar’s position as the global reserve currency.

The Founders intended for fiscal power to be exercised intentionally and with accountability. As Alexander Hamilton wrote in

Federalist No. 31:

A government ought to contain in itself every power requisite to the full accomplishment of the objects committed to its care, and to the complete execution of the trusts for which it is responsible, free from every other control but a regard to the public good and to the sense of the people.

As we enter our nation’s 250th year, we need to ask whether our fiscal policies live up to this ideal, and, if not, what change is required.