As the Senate steps up in the reconciliation process, there are still opportunities for savings before the final draft of the One Big Beautiful Bill is enacted into law. The House’s version of the reconciliation bill does make progress in reducing the cost of some energy tax credits through construction requirements and that progress should be locked in; however, many of the major tax credits still face long phase out times and there is still room to expand the construction requirements to more credits.

The IRA’s Expensive Subsidies

The House’s current version of the reconciliation bill includes changes to the Inflation Reduction Act (IRA)

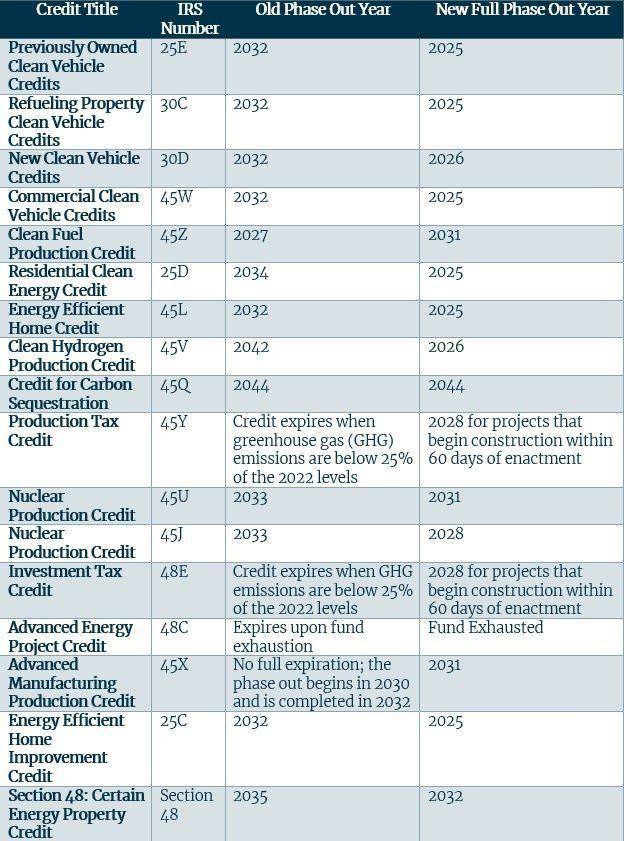

green energy tax credits. Under the IRA, most of the green energy tax credits were set to fully phase out between 2032 and whenever green house gases reached 25% below 2022 levels. The IRA credits would have cost

between $936 billion and $1.97 trillion and funded unsustainable energy sources at the expense of the American taxpayer.

The House originally proposed adjusting the phase out window to between the end of 2025 and 2044 for various credits as well as removing the ability for producers to transfer tax credits they earn. However, this original plan only provided

60% of the savings that a full repeal would have and left many of the tax credits for wind and solar intact long into the future.

In the bill that eventually passed the House, conservatives were able to negotiate faster phase out times for most credits and a requirement that projects seeking to qualify for the Investment Tax Credit (ITC) and the Production Tax Credit (PTC) must begin construction within 60 days of the enactment of the One Big Beautiful Bill.

Construction Requirements Create Savings

The construction requirement states that the ITC and PTC credits will terminate for any

qualified facility “the construction of which begins after the date which is 60 days after the date of the enactment of this subsection, or which is placed in service after December 31, 2028”. In this context,

beginning construction means either breaking ground on the site in question or incurring at least 5% of the total cost of the facility and receiving the components purchased. One or the other must occur within the 60 day window in order to have a chance of meeting the placed-in-service requirement.

A facility is considered to have been

placed-in-service when the project has reached a condition in which it is operable and available to produce and deliver energy or electricity.

While nuclear energy facilities have received a carve-out which permits them to start construction by the end of 2028 in order to be eligible for the tax credits, other types of energy facilities have not. Since the ITC and PTC have

primarily been used by wind and solar developers and beginning construction within 60 days is a difficult task, these two forms of energy production are likely to be the hardest hit by this new requirement.

These two energy sources are two of the most

problematic sources of energy for a reliable energy grid. Solar and wind are non-dispatchable energy sources which means that they can provide too much or too little energy depending on external conditions (usually weather). Non-dispatchable energy sources are intermittent and not predictable enough to build a stable energy grid off of and require base power loads such as nuclear, coal, or natural gas which are stable, dispatchable energy sources.

With that in mind, introducing construction requirements to the credits most relied on by unreliable energy sources while carving out credit opportunities for base power loads is a strategic win.

The House Makes Improvements to Some of the Major Cost Drivers

The major cost drivers of the IRA are the ITC, the PTC, the Advanced Manufacturing Production Credit, and the Credit for Carbon Sequestration.

One recent estimate from the Cato Institute places the cost of the combined ITC and the PTC at between

$70 and $180 billion per year by the time the greenhouse gas target could potentially be met. To combat this, the House implemented the construction and placed-in-service requirements for the ITC and PTC.

These construction requirements require that all new energy projects that would otherwise qualify for the ITC or PTC to begin construction within 60 days of the bill’s enactment and to begin production of electricity by the end of 2028. By including a carve-out for nuclear energy production facilities, the House ensured that for these credits only the most reliable sources of energy would be subsidized while those which can only provide an intermittent supply of energy are phased out.

The Advanced Manufacturing Tax Credit alone is projected by Credit Suisse to cost

$260 billion over the next decade due to the lack of caps and high take-up rate. The proposed bill text would wind down the eligible products that qualify for the tax credit. By 2027, wind production parts are no longer eligible and all other components (solar cells, batteries, inverters, critical minerals, etc.) would be phased down to zero in December 2031.

More Steps to Take on the Path to Savings

While these changes provide a meaningful step,

even greater savings are within reach if Congress addresses the Credit for Carbon Sequestration and extends the 60 day construction requirement to other credits.

The Credit for Carbon Sequestration (45Q) estimates have

increased dramatically from an initial

$3.23 billion over ten years per CBO to

$835 billion over the next decade based on a February estimate. The current bill text repeals the credit for foreign producers or “foreign-influenced entities”; however, the phase out date for domestic producers remains 2044. Congress should improve upon this by including a phase out date that is sooner.

The 60-day construction requirement is a vital first step in removing over-investment in wind and solar and restoring the

health of our energy grid. However, this should be extended to other production and manufacturing tax credits such as the Advanced Manufacturing Production Credit and the Clean Fuel Production Credit. If the final phase out dates are to remain in 2031, a construction requirement is necessary to encourage energy production that is financially responsible and does not profit off of taxpayer subsidies.

Congress should not let this opportunity pass them by and should instead use reconciliation to push for further energy reforms while protecting the House's good work in order to promote energy reliability and affordability for future generations.