The Congressional Budget Office (CBO) recently released its final tally of the federal government’s spending, revenues, and deficit for fiscal year (FY) 2023, which concluded in September 2023.

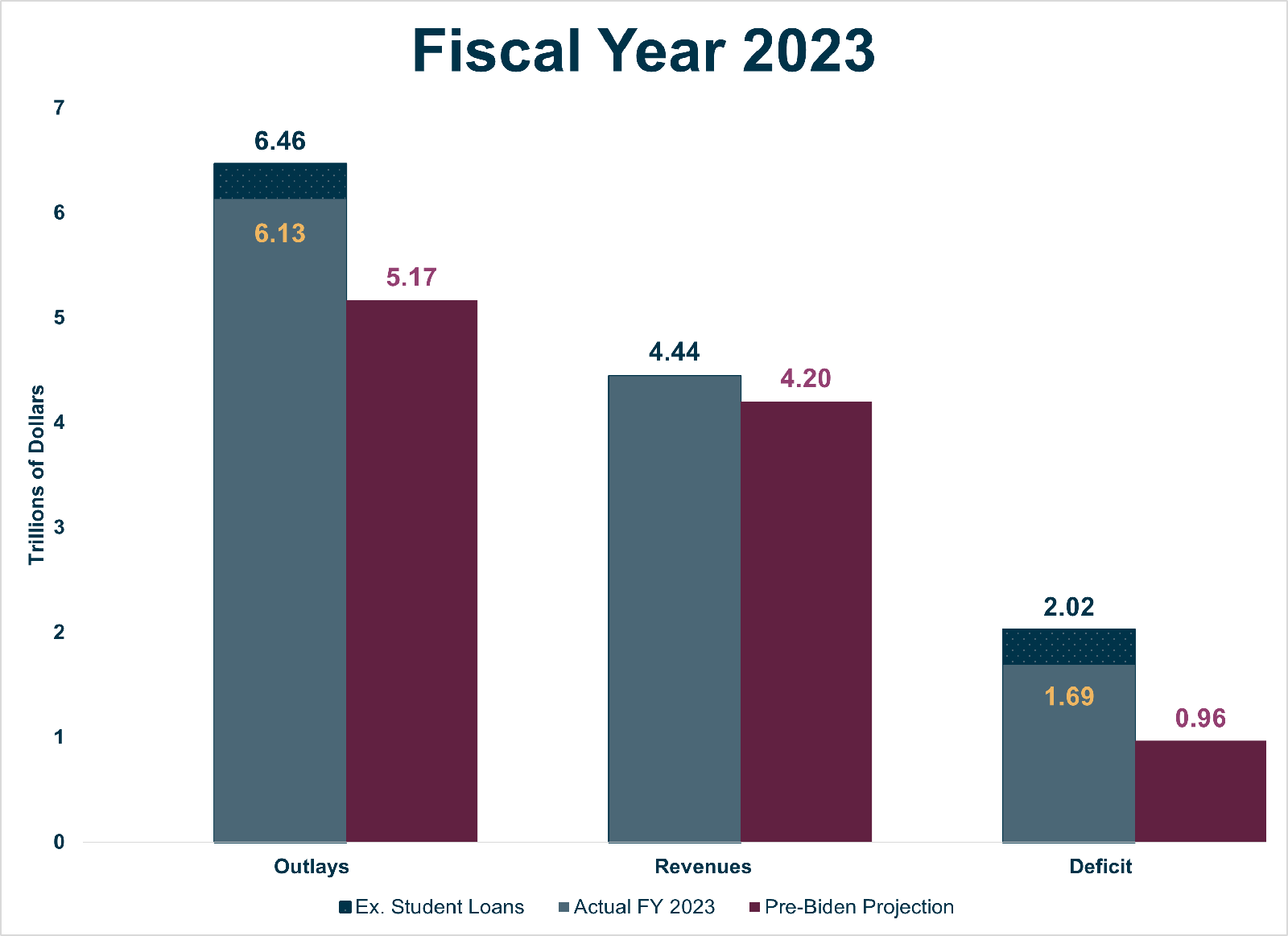

According to the CBO, FY 2023 outlays totaled $6.1 trillion and revenues were $4.4 trillion, resulting in a $1.7 trillion deficit.

The data underlying this report shows worrisome details, pointing to the need for policymakers to get serious about controlling spending.

FY 2023 Exceeds Pre-Biden Projections

The deficit is much higher than what had been projected before President Biden began to implement his policy agenda. Higher deficits are driven by actual spending being higher than originally estimated. These large deficits are despite revenues exceeding expectations and the large reduction in outlays recorded this year from the student loan decision.

Actual FY 2023 outlays are $966 billion above what CBO originally projected for the year when President Biden first came into office ($5.2 trillion). Revenues are $239 billion higher than projected ($4.2 trillion). The deficit is $727 billion higher than originally expected ($963 billion).

Excluding the effect of the Supreme Court’s student loan decision, the FY 2023 deficit was 110 percent higher than the CBO’s pre-Biden projection, with spending being 25 percent higher and revenues 6 percent higher.

Actual FY 2023 spending and the deficit are even worse than projected for that year by President Biden’s first budget request.

| FY 2023 Actual vs Biden’s First Budget (in trillions of dollars) | |||

| Outlays | Revenues | Deficit | |

| Biden Budget | 6.013 | 4.641 | 1.359 |

| Actual FY 2023 | 6.131 | 4.441 | 1.69 |

| Actual Ex. Student Loans | 6.464 | 4.441 | 2.023 |

| Actual vs Biden Budget | 0.118 | -0.2 | 0.331 |

| Actual Ex. Student Loans vs Biden Budget | 0.451 | -0.2 | 0.664 |

SCOTUS Student Loan Ruling Makes the Topline Look Better

The official topline spending and deficits levels in the CBO report look better due to the scorekeeping for the Supreme Court’s decision blocking President Biden’s student loan debt cancellation. This decision reduced both outlays and the deficit by $333 billion in FY 2023.

Scorekeeping for loan programs are governed by the Federal Credit Reform Act (FCRA). Unlike other spending (which is recorded on a cash basis when outlays actually occur), FCRA requires that the net present value of loans are recorded at the time a loan is made (or when a modification to the terms of the loan is made). Subsidized loans are recorded as outlays, while loans that turn a “profit” are offsetting receipts (negative spending).

In September 2022, President Biden announced the student loan cancellation scheme. Under FCRA rules, the taxpayer-financed subsidy costs of this loan cancellation were therefore booked as higher government spending in FY 2022.

After the Supreme Court struck down the plan, the $333 billion in lower outlays were accounted for in August 2023, reversing the deficit impacts from the prior year. Compared to FY 2022, CBO estimates that total U.S. Department of Education outlays were $680 billion less in FY 2023.

The Drivers of the Debt Problem Get Worse

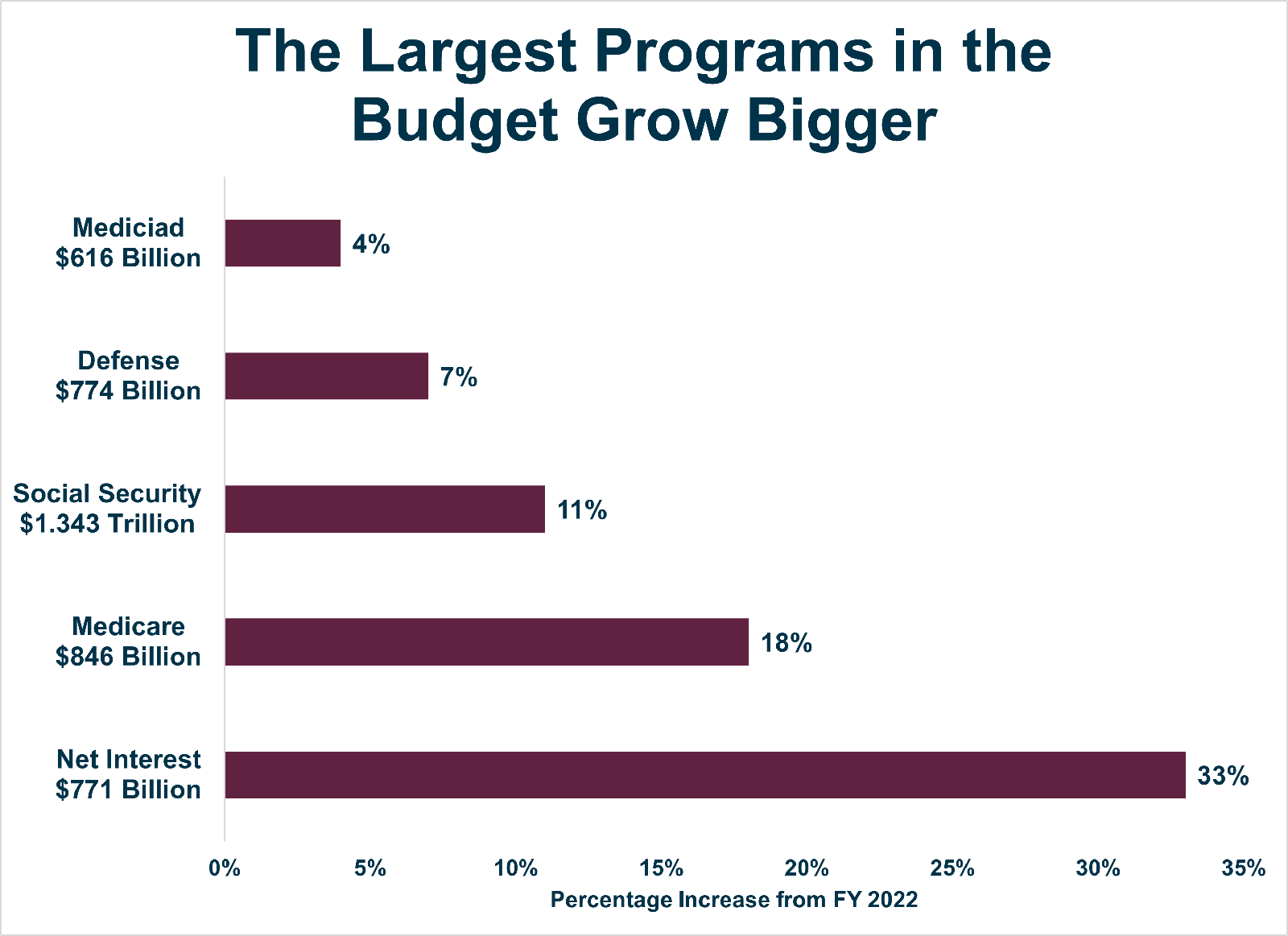

The five largest categories of the federal budget all grew significantly in FY 2023 from FY 2022. Interest payments on the debt increased 33 percent to $771 billion, Medicare increased 18 percent to $846 billion, Social Security increased 11 percent to $1.3 trillion, and Medicaid increased 4 percent to $616 billion.

These are also the programs that contribute the most to the government’s long term fiscal imbalance. As EPIC’s President & CEO Paul Winfree has shown, the two primary causes of projected debt accumulation over the next 30 years are federal health spending and interest payments. The growth of this spending will erode the government’s “fiscal space,” which could threaten its ability to borrow further.

Time to Get Serious About Controlling Spending

This CBO report should be an alarm bell for Congress and the White House.

Washington’s spending binge has produced high inflation. Excessive government spending and large deficits crowd out private investment, making our economy less resilient and jeopardizing the prosperity of American families.

The time to address Washington’s spending binge has come.