President Joe Biden has repeatedly claimed that his policies have reduced the deficit. In reality, his Administration has made the fiscal trajectory even less sustainable by increasing government spending and the deficit. Even The Washington Post gave President Biden’s claim a “Bottomless Pinocchio” rating.

[1]

Real wages for the average American worker are 4.5 percent lower today than they were in January 2021 as a result of high inflation, making the typical employee about $2,700 worse off.

[2] This inflation was produced by trillions of dollars in higher government spending, much of which was financed by newly printed money by the Federal Reserve.

To make better decisions, policymakers should review how the country reached this point and compare it to alternative paths that could have been taken.

A logical approach to gauge the outcomes of Bidenomics is to compare the actual results to what analysts expected prior to the enactment of the Biden policies. The Congressional Budget Office’s (CBO’s) February 2021

Budget and Economic Outlook projections provides a useful baseline against which to measure the effects of President Biden’s policies. This CBO

Outlook was released on February 11, 2021, just 22 days after President Biden’s inauguration. The CBO based its fiscal and economic projections on the laws in effect as of January 12, 2021, providing a clean slate just prior to any of President Biden’s policy agenda being enacted.

[3] (Data from the February CBO baseline is referred to here as the “pre-Biden baseline.”)

Higher Deficit and Debt

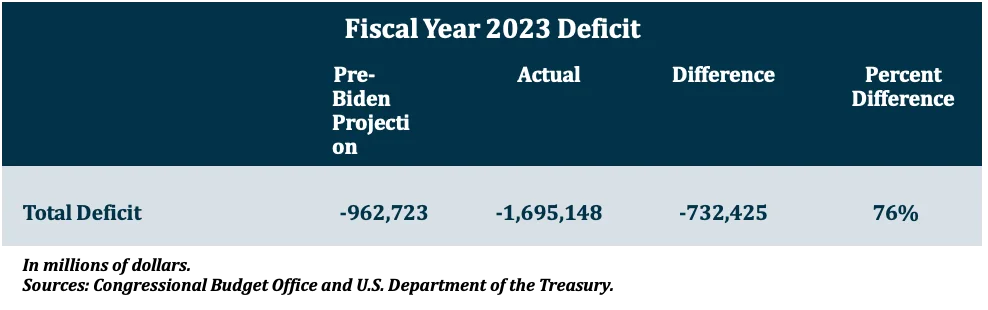

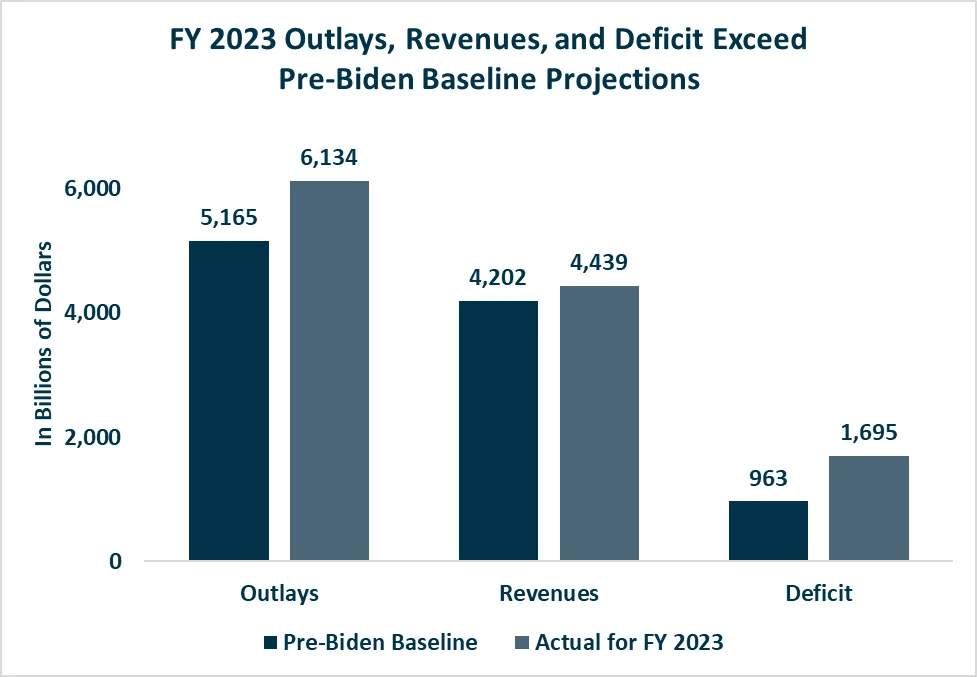

The pre-Biden baseline projected that the deficit for FY 2023 would be $962.7 billion. The actual FY 2023 deficit was $1.695 trillion, 76 percent higher than the amount projected.

[4]

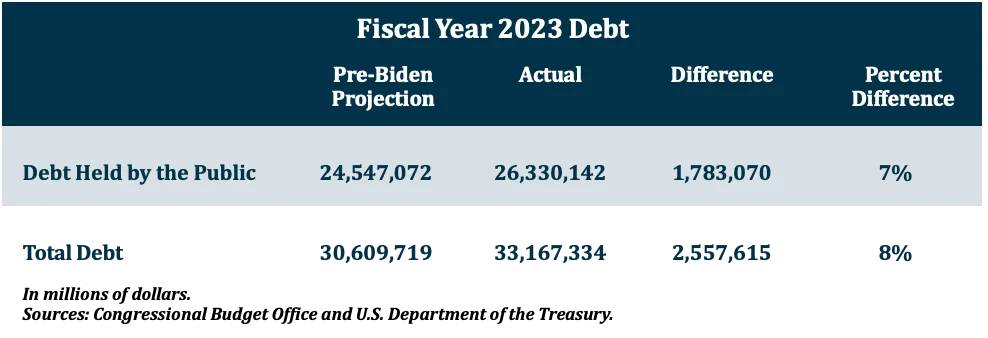

The national debt is also much higher than the CBO forecast prior to enactment of Biden’s policy agenda. The pre-Biden baseline projected that debt held by the public would be $24.547 trillion at the end of FY 2023, while the actual figure was $26.33 trillion, $1.783 trillion higher than projected. The total national debt (including intergovernmental debt) exceeded expectations even further, coming in at $2.558 trillion above the pre-Biden baseline to reach $33.167 trillion at the end of FY 2023.

Higher Spending Explains the Entirety of the Deficit Increase in FY 2023 Relative to Projections

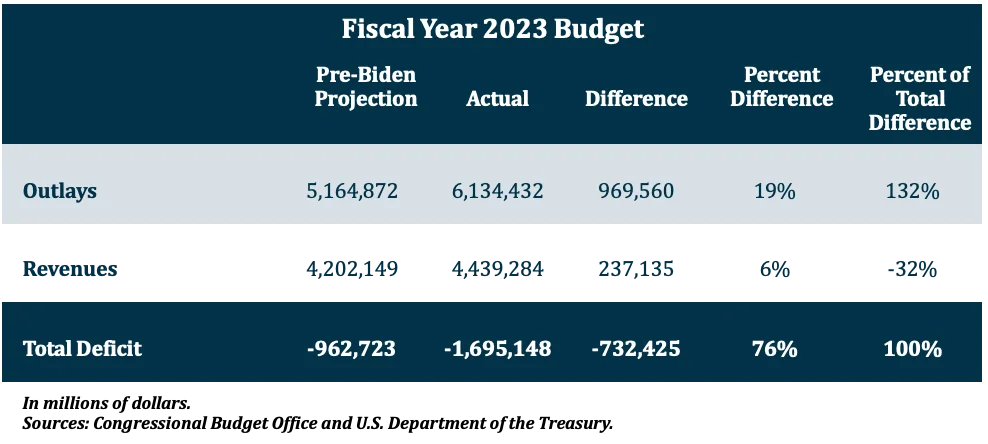

The entire increase in the actual FY 2023 deficit compared to the pre-Biden projection is attributable to outlays significantly exceeding expectations.

Actual FY 2023 outlays were $969.6 billion above the pre-Biden baseline, an increase of 19 percent above the projection.

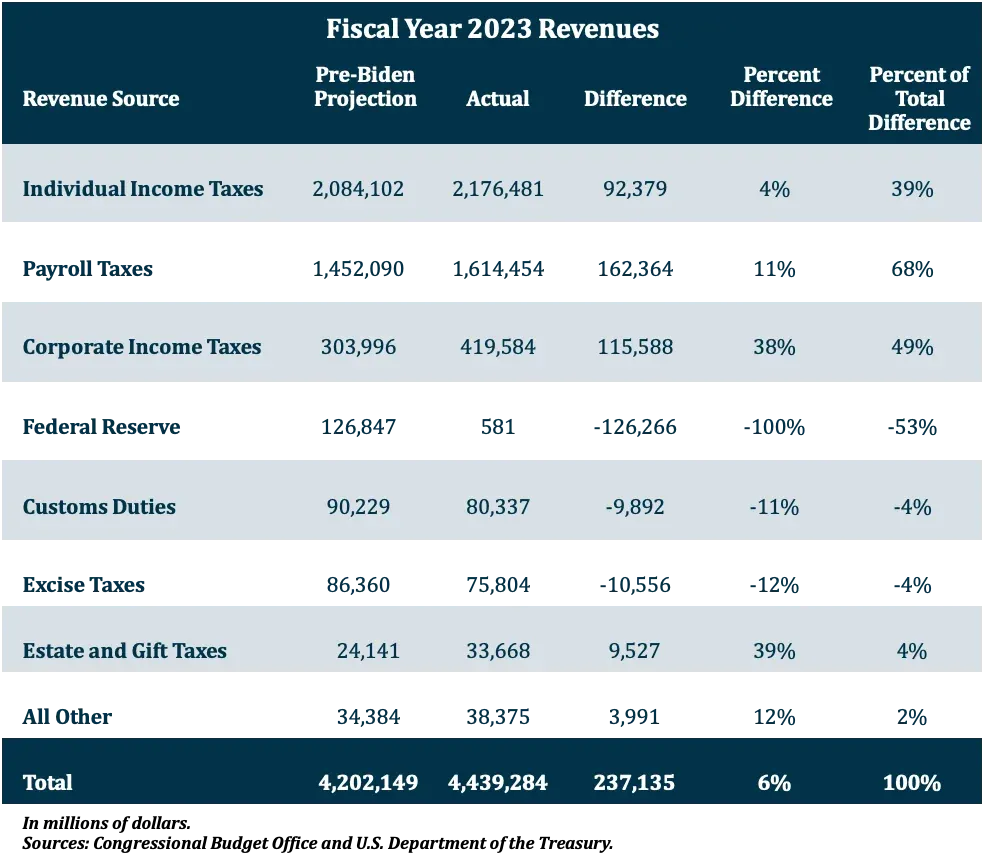

The deficit increase above the pre-Biden baseline was partially offset by actual revenues exceeding the pre-Biden baseline. Actual revenues were $237.1 billion (6 percent) higher than the pre-Biden projection.

Biden Policies Drive Spending Increases

The causes of increases in actual spending relative to the pre-Biden baseline generally fall into two categories:

Policy Choices Made by President Biden and Congress to Intentionally Increase Spending.

President Biden made increasing government spending a top priority for his Administration. Until this year, Congress was happy to oblige with trillions in higher spending. The initial $1.9 trillion American Rescue Plan Act was followed by the massive Infrastructure and Jobs Act, the misnamed Inflation Reduction Act, the Honoring our Promise to Adress Comprehensive Toxins (PACT) Act, the Creating Helpful Incentives to Produce Semiconductors (CHIPS) and Science Act, supplemental spending related to Ukraine, and large increases to the regular discretionary appropriations for FY 2022 and FY 2023.

[5]

President Biden increased spending via executive actions even when Congress did not grant authority to do so. According to the House Budget Committee, the fiscal costs of Biden Administration executive actions has exceeded $1 trillion, including hundreds of billions in student loan forgiveness, expanding Obamacare, and unilaterally increasing food stamp benefits.

[6]

Programs that Are Sensitive to Inflation.

This excessive spending produced high inflation. The CBO originally projected that the consumer price index(CPI-U) would grow about 5.6 percent between January 2021 and September 2023. In reality, prices rose by 17.7 percent.

[7], ” retrieved from FRED, Federal Reserve Bank of St. Louis;

https://fred.stlouisfed.org/series/CPIAUCNS (accessed October 27, 2023).]

Inflation had a feedback effect into the federal budget, driving spending even higher. Programs such as Social Security automatically increase each year with inflation. In particular, net interest payments to finance the deficit skyrocketed as interest rates rose and the primary deficit increased.

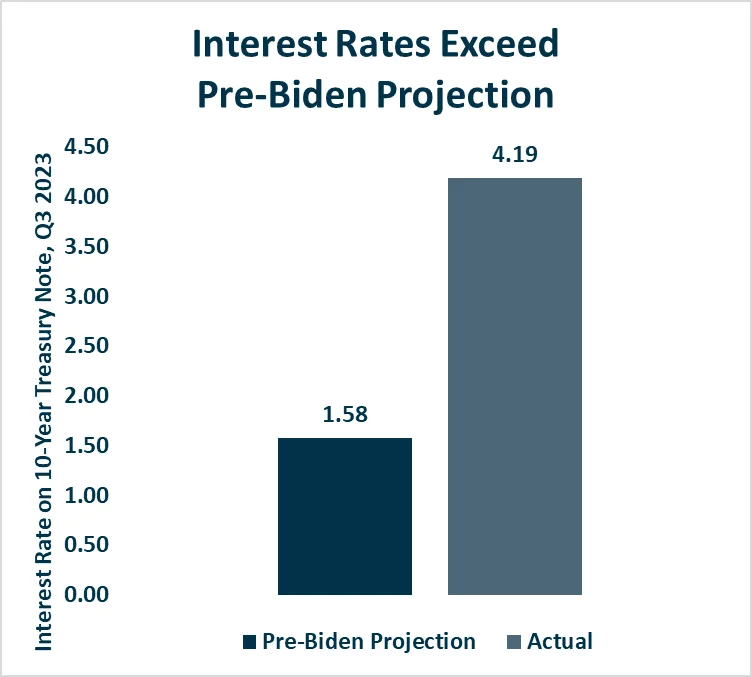

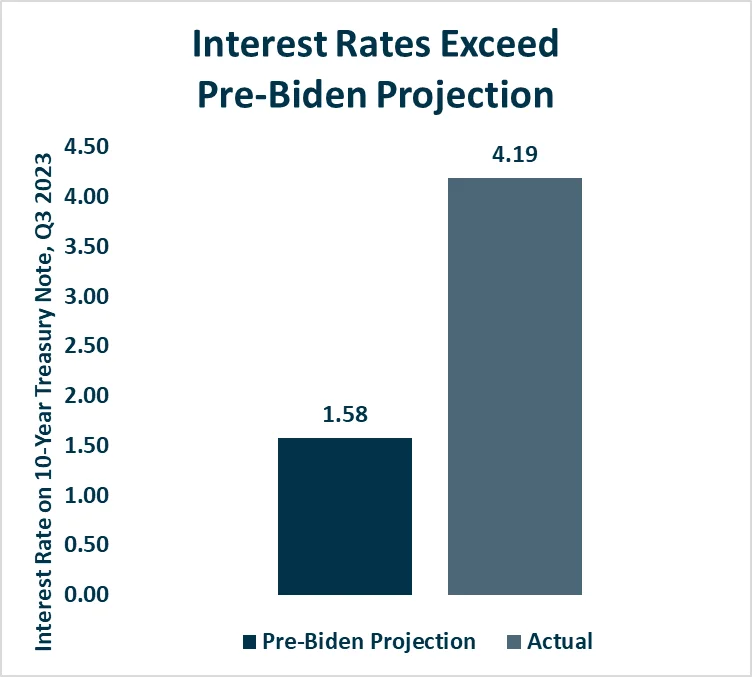

Higher net interest costs were the most significant factor, accounting for 39.3 percent of the total increase in higher FY 2023 outlays above the pre-Biden baseline. Interest costs were 137 percent higher than projected due to both higher debt and higher interest rates on the national debt. The CBO's pre-Biden projection for the interest rate on 10-year Treasury Notes for the third quarter of 2023 was 1.576 percent. The actual average 10-year interest rate for the third quarter of 2023 was 4.19 percent.

[8],” retrieved from FRED, Federal Reserve Bank of St. Louis,

https://fred.stlouisfed.org/series/DGS10 (accessed October 23, 2023).]

Other significant contributors to higher-than-projected spending included Medicaid ($124 billion above pre-Biden baseline), the FDIC Deposit Insurance Fund ($97 billion above pre-Biden baseline), Social Security ($79 billion above pre-Biden baseline), and food stamps ($57 billion above pre-Biden baseline).

The two appendices at the end of this report provide a more detailed review of the differences in actual and projected program spending and the causes of spending increases for certain programs.

Revenues Exceed Projections

Revenues were $237.1 billion higher in FY 2023 than the pre-Biden projection, an increase of 6 percent.

Individual income taxes, payroll taxes, and corporate income taxes range from 4 percent to 38 percent higher than the pre-Biden projection.

Conversely, actual remittances from the Federal Reserve were more than $126 billion below the pre- Biden projection, falling to just $581 million in FY 2023. This is a result of the Federal Reserve’s fourth round of quantitative easing (QE4) in which it bought significant quantities of low interest debt with yields that are now below the interest rates that the Federal Reserve is now paying on its liabilities. Under normal circumstances, the Federal Reserve remits its operating profits to the Treasury, which are recorded as revenues. However, since the Federal Reserve is now operating at a loss, remittances have largely been suspended.

[9]

Supreme Court Decision on Student Loans Partially Mitigates the Deficit Increase

As bad as the actual FY 2023 deficit was, it is important to remember that President Biden wanted spending to be hundreds of billions higher.

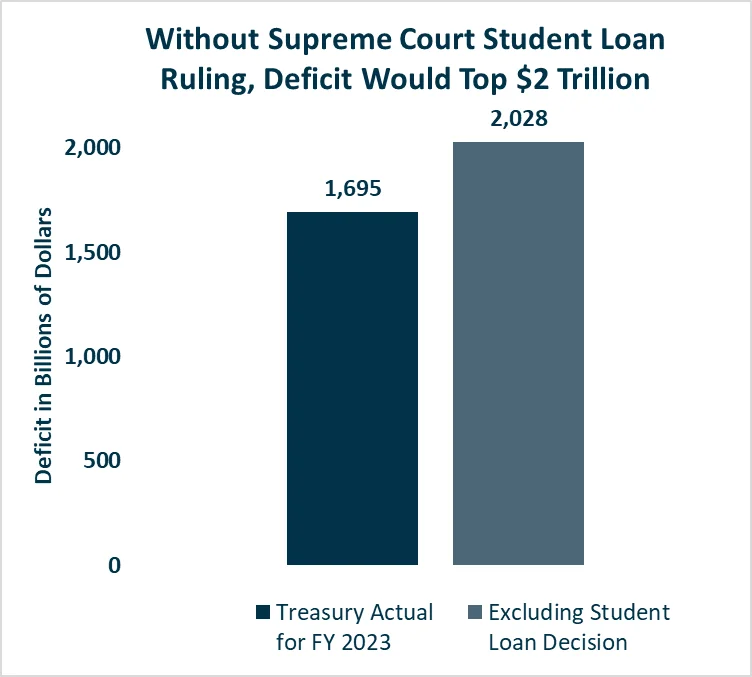

In September 2022, President Biden announced his student loan cancellation scheme, which would have forgiven up to $20,000 in U.S. Department of Education loans for certain individuals. However, the Supreme Court rightly invalidated the plan in 2023. The resulting $333 billion in lower outlays— attributable to borrowers paying the balances of their loans rather than taxpayers—were accounted for in the CBO’s August 2023 update.

[10]

After the Supreme Court ruling invalidating the debt cancelation plan, the Biden Administration finalized a rule creating a new income-driven repayment (IDR) student loan plan, called Saving on a Valuable Education (SAVE).

[11]

The net effect of the Supreme Court decision and the IDR rule reduced actual outlays by $204 billion in FY 2023. The lower-than-projected outlays for student loan programs mitigated 20.5 percent of the total increase in outlays above the pre-Biden baseline.

Without the Supreme Court decision, total FY 2023 outlays would have been $6.467 trillion, resulting in a $2.028 trillion deficit. That level of spending would have been $1.3 trillion higher than the pre- Biden baseline. The deficit would have been $1.065 trillion higher than projected.

Biden Officials’ Misleading Deficit Blame Game

In releasing the final FY 2023 budget data, Secretary of the Treasury Janet Yellen and Office of Management and Budget (OMB) Director Shalanda Young blamed the deficit problem on lackluster revenues, stating:

- Falling revenues are a significant contributor to the 2023 deficit, underscoring the

importance of President Biden’s enacted and proposed policies to reform the tax system.

- After atypically strong growth in revenues in 2022, driven by record-high capital gains

receipts and the historic recovery from the pandemic, revenues in 2023 fell to 16.5 percent of gross domestic product (GDP), with individual and corporate receipts returning to lower levels in line with projections made after the passage of the Tax Cuts and Jobs Act of 2017. This drop in revenues was the primary driver of the increase in the deficit as a share of GDP. By contrast, non-interest spending did not meaningfully contribute to the increase in the deficit as a share of GDP.[12]

It is true that revenues in FY 2023 were lower than in FY 2022. After hitting record levels in 2022, tax collections dipped in 2023 as a result of reduced capital gains realizations, decreased remittances from the Federal Reserve, and higher tax credit claims.

However, as this report shows, actual revenues in FY 2023 were hundreds of billions higher than projected by the CBO prior to President Biden’s policies taking effect. A lack of revenue is not the reason for the growing deficit.

It is misleading to claim that “non-interest spending did not meaningfully contribute to the increase in the deficit.” As this report shows, net interest outlays account for 39.3 percent of the total increase in higher outlays above the pre-Biden baseline for FY 2023. The remaining 60.7 percent of the increase in outlays was non-interest spending. Furthermore, one of the factors contributing to rising net interest costs is the higher primary deficit that is driven by increasing non-interest spending.

Reversing the Harm of Reckless Spending

It is clear that the policies of the Biden Administration have put the federal budget on a less sustainable path. Despite President Biden’s claims to have reduced the deficit, the actual deficit in FY 2023 was 76 percent higher than projected by the CBO before his policy agenda was enacted.

The higher-than-projected deficit occurred despite actual revenues being $237.1 billion above the pre-Biden projection. The entire increase in the deficit is due to actual FY 2023 outlays being nearly

$1 trillion higher than expected prior to enactment of President Biden’s policies.

FY 2023 outlays were $969.6 billion higher than the pre-Biden projection as a result of policy choices made by President Biden and Congress to intentionally increase spending as well as the high inflation that resulted from excessive government spending.

To correct the course and put the government on a more sustainable fiscal trajectory, lawmakers should:

- Do no more harm - Washington’s reckless spending binge has produced inflation rates that had not been seen in the United States in four decades. Rejecting new proposals to further increase spending

should be common sense.

- Take steps to control spending - Under the current baseline assumptions, federal government spending is projected to increase from 22.7 percent of GDP in 2023 to 24.8 percent of GDP by 2033 and then continue growing to 29.1 percent of GDP in three decades. This growing spending would push the debt held by the public from about 98 percent of GDP today to 181 percent of GDP in 2053. This fiscal path would not be sustainable and risks exhausting the fiscal space for the federal government to finance additional obligations, which would cause a fiscal crisis. The only way to head that scenario off is for lawmakers to proactively make changes to spending programs to ensure that they do not grow faster than the economy.

American families are suffering from lower real wages due to the inflation produced by too much government spending. It is far past time for lawmakers to get serious about addressing the underlying causes of the problem.

Appendix I: Differences Between Actual FY 2023 Outlays and the Pre-Biden Baseline

The table below provides a summary of the differences in actual FY 2023 outlays with the pre-Biden baseline for significant budget functions, accounts, and programs.

Appendix II: The Causes of Significant Spending Increases

This appendix describes the underlying factors of selected programs that drove the increases in spending.

Net Interest Costs Rise.

Higher net interest costs were the single most significant factor in the actual FY 2023 deficit increase over the pre-Biden CBO baseline.

Actual net interest payments totaled $659.2 billion in FY 2023; a total that was $380.7 (137 percent) higher than the pre-Biden baseline projection of $278.5 billion. The increase in net interest costs accounted for 39.3 percent of the total increase in higher outlays above the pre-Biden baseline.

Net interest costs were higher than projected due to both a higher principal and higher interest rates on the national debt.

The actual FY 2023 primary deficit (the gap between revenues and spending that needs to be financed by debt) was $351.7 billion (51 percent) higher than the pre-Biden baseline projection. This larger primary deficit is entirely attributable to non-interest outlays being $588.9 billion higher than projected.

The CBO pre-Biden projection for the interest rate on 10-year Treasury Notes for the third quarter of 2023 was 1.576 percent. The actual average 10-year interest rate for the third quarter of 2023 was 4.19 percent.

[13],” retrieved from FRED, Federal Reserve Bank of St. Louis,

https://fred.stlouisfed.org/series/DGS10 (accessed October 23, 2023).]

Medicaid Expansions.

Actual Medicaid outlays in FY 2023 were $615.8 billion, $123.9 billion (25 percent) above the pre-Biden projection of $491.9 billion. The increase in Medicaid spending accounted for 12.8 percent of the total increase in outlays above the pre-Biden baseline.

Between January 2021 and June 2023 (the most recent data available), Medicaid enrollment grew by nearly 12 million individuals (16 percent) to 85.6 million.

[14] The increase in enrollment is due primarily to the “continuous enrollment provision,” which increased the federal matching rate by 6.2 percentage points to states that did not remove ineligible beneficiaries from Medicaid coverage while a public health emergency declaration was in effect. The public health emergency declaration was extended several times by the Biden Administration, even after President Biden himself said “the pandemic is over.” The restriction on eligibility redeterminations continued until April 2023, while the enhanced federal funding was extended at phased-down rates through the end of 2023.

FDIC and Bank Failures.

Actual outlays from the Federal Deposit Insurance Corporation (FDIC) Fund totaled $91.7 billion in FY 2023, a $97 billion (1,830 percent) increase above the pre-Biden projection (the Deposit Insurance Fund normally collects more in assessments, which are recorded as offsetting collections or negative outlays, than it spends out in payments). The higher Deposit Insurance Fund spending accounted for 10 percent of the total increase in higher outlays above the pre-Biden baseline.

Bank deposits up to $250,000 are guaranteed by payments from the Deposit Insurance Fund. Three of the four largest bank failures in U.S. history occurred in 2023, with First Republic Bank, Silicon Valley Bank, and Signature Bank entering FDIC receivership. The FDIC made a systemic risk exception to the $250,000 deposit insurance limit and instead guaranteed all deposits at Silicon Valley Bank and Signature Bank. According to the Treasury Department, the FDIC made a $49.4 billion transaction in September 2023 with the Federal Financing Bank related to the receivership of First Republic Bank.

[15]

The rapid rise in interest rates in response to high inflation contributed to the failures of these financial institutions.

Social Security COLA.

Actual Social Security spending in FY 2023 totaled $1.354 trillion, $78.7 billion (6 percent) higher than the pre-Biden projection of $1.276 trillion. The higher Social Security spending accounted for 8.1 percent of the total increase in higher outlays above the pre-Biden baseline.

Social Security is sensitive to inflation, as it provides a cost-of-living adjustment (COLA) for benefits each year. The COLA was 8.7 percent for calendar year 2023 and 5.9 percent for 2022.

Food Stamp Benefit Increases.

Actual spending for the Supplemental Nutrition Assistance Program (SNAP, commonly called food stamps) in FY 2023 was $134.3 billion, 73 percent ($57 billion) higher than the pre-Biden baseline projection of $77.7 billion. The increase in food stamp spending accounted for 5.9 percent of the total increase in outlays above the pre-Biden baseline.

Actual average monthly participation in food stamps was similar to the pre-Biden projection of 42.3 million. However, the actual average monthly benefit in FY 2023 was 57 percent higher than the pre- Biden projection. Benefit levels were higher primarily as a result of two policies implemented by President Biden's Administration.

In 2021, the Biden Administration unilaterally increased the Thrifty Food Plan calculation, which is used to determine food stamp benefit levels, in defiance of congressional intent and nearly 50 years of precedent. The CBO estimated that the increase in food stamp benefits by executive action could cost up to $300 billion over 10 years, and the Government Accountability Office (GAO) found that the Biden Administration violated the Congressional Review Act and failed to meet basic standards.

[16]

Food stamp emergency allotments were originally provided during the COVID-19 pandemic and allowed to remain in effect during the declaration of a public health emergency. The public health emergency declaration was extended several times by the Biden Administration, even after President Biden said “the pandemic is over.” The emergency allotments finally ended in March 2023.

Defense and International Security Assistance for Ukraine.

National defense outlays totaled $820.7 billion in FY 2023, $50.7 billion (7 percent) higher than the pre-Biden projection of $770.1 billion.

International Security Assistance Program outlays totaled $29.2 billion; $17.5 billion (151 percent) higher than the pre-Biden baseline of $11.5 billion.

Together, the $68.2 billion in higher-than-projected Defense and International Assistance outlays accounted for 7 percent of the total increase in outlays above the pre-Biden baseline.

Aid to Ukraine is a significant contributor to the increase in Defense and International Assistance outlays in FY 2023 relative to the pre-Biden projection. Since March 2022, $113 billion has been appropriated for military and assistance related to the Russian invasion of Ukraine. The majority of funding has been for the Department of Defense, which has received $61.8 billion. The USAID Economic Support Fund has received $27 billion.

[17]

PBGC and Union Pension Bailouts. Actual outlays from the Pension Benefit Guaranty Corporation (PBGC) fund in FY 2023 totaled $40.2 billion, $46.3 billion (754 percent) higher than the pre-Biden projection (the PBGC normally collects more in premiums, which are recorded as offsetting collections or negative outlays, than it spends out in payments). The increased spending from the PBGC fund accounted for 4.8 percent of the total increase in outlays above the pre-Biden baseline.

President Biden’s American Rescue Plan Act included a massive taxpayer-funded bailout for poorly managed union pension plans. Even after this bailout, Senate Democrats were able to push the PBGC to make the funding for the union plans more generous, costing taxpayers billions more.

[18]

Veterans Benefit Increases.

Actual outlays for Veterans Benefits and Services totaled $301.6 billion in FY 2023, $43 billion (17 percent) above the pre-Biden baseline. The higher veterans spending accounted for 4.4 percent of the total increase in outlays above the pre-Biden baseline.

The Honoring our PACT Act of 2022 was enacted in August 2022. This legislation significantly increased spending on veterans programs, including the creation of the Toxic Exposures Fund. The CBO has said that the PACT Act will increase deficits by $797 billion over the 2022–2032 period.

[19]

Obamacare Subsidies Expansions.

Refundable premium tax credits under the misnamed Affordable Care Act totaled $82.6 billion in actual outlays in FY 2023, $35.1 billion (74 percent) higher than the pre-Biden baseline. The higher spending for these Obamacare subsidies accounted for 3.6 percent of the total increase in outlays above the pre-Biden baseline.

President Biden’s American Rescue Plan Act significantly expanded the Obamacare subsidies, including by eliminating the maximum income for eligibility for taxpayer subsidies. The Inflation Reduction Act of 2022 extended the expanded subsidies through 2025.

Transportation Spending Increases.

Actual outlays for transportation programs totaled $127.2 billion in FY 2023, $21.5 billion (20 percent) higher than the pre-Biden baseline. The increase in transportation spending accounted for 2.2 percent of the total increase in outlays above the pre-Biden baseline.

The Infrastructure Investment and Jobs Act of 2021 was enacted in November 2021. This legislation was meant to significantly increase spending on transportation infrastructure as well as on green energy, climate programs, and broadband infrastructure over a five-year period.