What is the Convenience Yield?

Since World War II, debt issued by the U.S. Treasury has been considered the worldwide safe asset. Investors around the world want to hold U.S. government debt because it is expected to be repaid in full, highly liquid, and denominated in dollars, reflecting its status as the reserve currency.

Investors pay for this perceived safety by accepting a lower interest rate on U.S. Treasury debt, known as the convenience yield.

The convenience yield can be considered a subsidy paid to the U.S. Treasury by the rest of the world in exchange for providing the safe asset. This special status, sometimes referred to as the “exorbitant privilege,” has allowed the federal government to finance its deficit spending more cheaply than it otherwise would have.

The country that is considered to provide the safe asset

gains the ability to borrow beyond what its fiscal fundamentals would support. However, if the underlying fiscal position deteriorates, the exorbitant privilege can be lost. While the United Kingdom enjoyed the convenience yield prior to World War I, it lost that special status to the United States.

The Convenience Yield is Evaporating

The convenience yield on U.S. Treasuries has been falling.

Government spending is

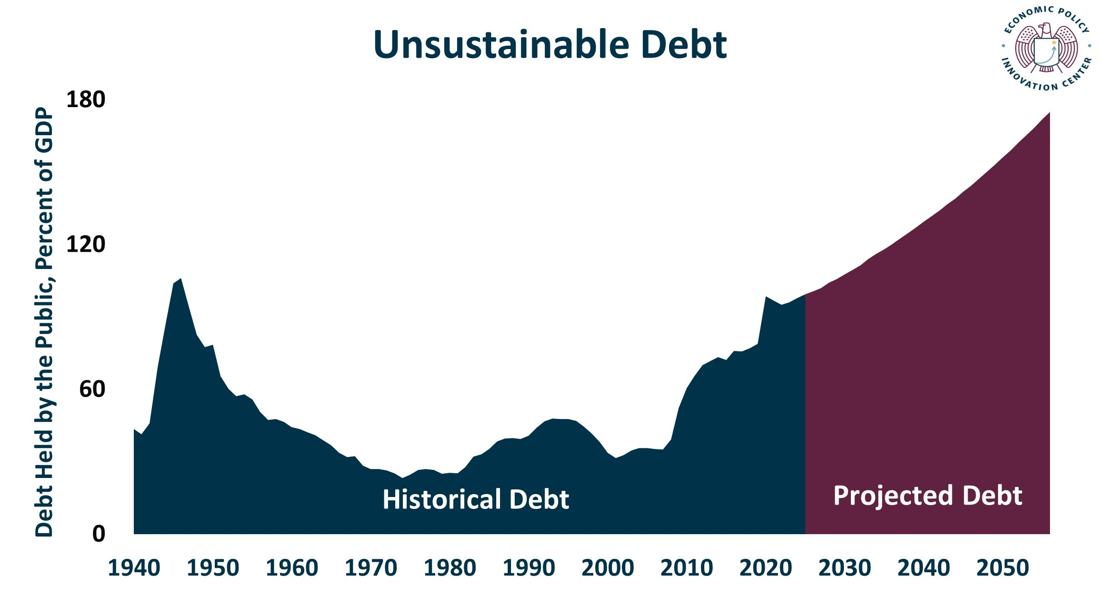

growing faster than the economy, which is inherently unsustainable. Declining fiscal space is sending a signal to the markets that U.S. debt is not as safe as it has been. Excessive supply of U.S. Treasury debt is outpacing demand.

Jiang, Richmond, and Zhang (2025) observe “that there is a clear negative relationship between convenience yields and outstanding Treasury quantities.”

Du et al. (2025) “find that increases in the U.S. debt-to-GDP ratio are systematically associated with lower U.S. Treasury convenience across maturities… These findings suggest that the large increase in U.S. Treasury issuance has played a central role in the waning convenience yield of U.S. government bonds.”

Several economists estimate that the convenience yield has recently turned negative, suggesting that the special status of U.S. government debt may no longer exist, especially at longer maturities.

- Du et al. (2025) found that “The U.S. Treasury convenience has continued its secular decline since the aftermath of the GFC [2008 Global Financial Crisis] and is now strongly negative vis-à-vis government bonds denominated in G10 currencies. For the first time, the short-term (3-month and 1-year) U.S. Treasury convenience also become largely negative since 2023.”

- Jiang, Richmond, and Zhang (2025) show “convenience yields on U.S. Treasurys have declined in recent years, turning negative across several maturities… The 10- year Treasury convenience yield is around −0.25 percent at the end of our sample, and the 1-year Treasury convenience yield is close to 0…“While the U.S. has been benefiting from issuing debt at lower interest rates, our evidence indicates that this advantage is increasingly limited to short-term debt, with negative yields on long-term debt signaling potential limits to the global market’s capacity to absorb U.S. debt.”

Research suggests the April 2025 tariff shock further reduced the convenience yield:

- Acharya and Laarits (2025) “document that such convenience yields of long-term bonds saw marked decreases at the onset of the Tariff War, in contrast to short-term convenience yields that appreciated with heightened uncertainty brought on by tariff news.”

- Jiang et al. (2025) found that, using high frequency data in the aftermath of the tariff announcement, “Investors’ demand for the canonical dollar-denominated safe asset, U.S. Treasurys, has declined. Foreign investors no longer seem willing to pay extra for the safety and liquidity of Treasurys, and indeed they favor the German Bund over the Treasury bond.”

What Would be the Costs of Losing the Convenience Yield?

Losing the convenience yield would be extremely costly for taxpayers and consumers.

A collapse in the convenience yield could increase the natural rate of interest (denoted as

r*), which is the neutral real interest rate that is neither stimulative nor restrictive of economic growth. The natural rate of interest has fallen steadily over the last several decades; however, an uptick has recently been observed coinciding with the falling convenience yield. Recent

research shows that changes in the convenience yield can affect

r* quickly and substantially. If the natural rate of interest increases, that would lead the Federal Reserve to keep interest rates higher, raise the cost of financing the national debt, and increase the cost of mortgages and business investment.

Calculations of the historical convenience yield enjoyed by the U.S. Treasury can vary based on methodology and the maturity of the debt. Some recent estimates include:

If interest rates are persistently 50 basis points higher than baseline projections, it would add $1.9 trillion to the deficit over the next decade, based on data from the

Congressional Budget Office (CBO). In this scenario, the net interest costs in FY 2036 would be about $2.5 trillion, 15% ($312 billion) higher than the CBO’s baseline projection.

Rising net interest costs would accelerate the depletion of the government’s fiscal space. This would weaken the government’s

ability to respond to emergencies as its borrowing capacity is reduced.

As the safety of U.S. government debt comes into question, the dollar’s status as the reserve currency of the world could also be challenged, as

historically “the reserve currency has always been housed in the country with the largest supply of safe and liquid government assets.” However, there is

recent evidence that although the convenience yield on U.S. Treasury debt has fallen, confidence in the dollar has remained strong.

How Should Congress React to the Falling Convenience Yield?

To restore and preserve the convenience yield, Congress needs to reduce the supply of new debt. Simply put, Congress needs to reduce the deficit by

reducing government spending.

Lawmakers should also seek clarity from the CBO about how its assumptions account for the convenience yield in the budget baseline as well as the potential fiscal and economic costs of losing the exorbitant privilege.