On Sunday, November 9, 2025, the Senate Appropriations Committee released text for three fiscal year 2026 (FY) appropriations bills:

Agriculture-FDA,

Legislative Branch, and

Military Construction and Veterans Affairs. These bills were then packaged together with a Continuing Resolution to end the

government shutdown.

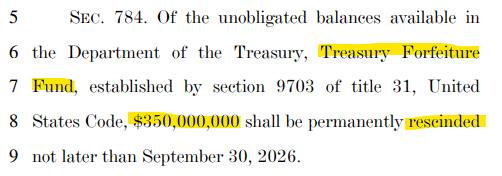

While the text for the three FY 2026 bills largely mirrors what the Senate Appropriations Committee produced over the summer, there are some noteworthy differences. One of these is

Section 784 of the Agriculture-FDA bill, which was not present in any form of the previous FY 2026 House or Senate bills. The provision is a budget gimmick carefully designed to avoid scrutiny.

Treasury Forfeiture Fund & CHIMPs

Section 784 rescinds $350 million from the

Treasury Forfeiture Fund (TFF), which is funded by proceeds from certain law enforcement activities. These receipts are used to reimburse federal, state, and local law enforcement agencies for pertinent expenses, and the TFF often takes in more money than the expenses require.

The Senate’s revised FY 2026 Agriculture bill would rescind $350 million from the TFF.

This is not the first TFF rescission Congress has proposed. The

second FY 2024 appropriations package contained two TFF rescissions worth a combined $647.5 million, and there are many instances of the rescission from previous years.

Although the TFF is typically addressed as part of Financial Services and General Government appropriations bill (which covers the U.S. Department of the Treasury), TFF rescissions can be coupled with unrelated agencies such as the U.S. Department of Agriculture. For example, the second of the FY 2024 TFF rescissions was placed in the U.S. Department of State division of the bill.

The TFF rescission is part of a category of policies known as

Changes in Mandatory Programs (CHIMPs). While appropriations bills focus on the

discretionary budget category, these bills can adjust the mandatory spending category as well. Such changes are scored by the Congressional Budget Office (CBO), and the effects are counted towards discretionary spending caps.

Given that discretionary spending limits are contested, whereas mandatory spending lacks any meaningful constraint, CHIMPs are typically policy changes that reduce budget authority (BA). The standard practice is for appropriators use CHIMPs as an “offset” on paper, meaning that the BA savings from the CHIMP creates room for additional spending elsewhere in the bill while technically staying within the limit.

False “Savings” from CHIMPs & The Unicorn Gimmick

Legislators should know that not all BA reductions are equal. This is because BA is an upper limit to spending, and not all BA is translated into outlays (OT).

The TFF is a program that has a consistent gap between BA and OT. Law enforcement is authorized to use TFF funds, but there is typically a leftover amount that is unspent – meaning the OT is less than the BA. Appropriators are careful not to make TFF rescissions large enough to disrupt allowable law enforcement spending, instead targeting what would be “excess” BA that expires at the end of the fiscal year.

However, rescinding “excess” BA is not a proper budgetary offset. This is because the goal of offsets is to reduce deficits, and deficits are caused by overspending. CHIMPs become a budget gimmick by trading BA that would result in no new spending for BA in other accounts that will generate new spending.

An analogous situation at the household level would be if a family member requested $350,000 to buy a unicorn. Since unicorns do not exist, this silly request is granted. The family member then cancels the unicorn request and buys a luxury car, leaving the household with $350,000 in new debt. It would not be credible to claim that the unicorn cancellation made the luxury car purchase financially responsible, because the “authority” to buy a unicorn was never going to lead to spending. Instead, the unicorn request was a budgetary gimmick meant to enable buying the luxury car.

In the case of the TFF rescission, the $350 million in false savings is used to artificially lower the on-paper BA of the Agriculture bill, making it appear more modest than it is.

Scorekeeping Behind Closed Doors

The use of CHIMP gimmicks is aided by scorekeeping rules that benefit appropriators.

CBO scores for most pending legislation are

posted on its website, often with a significant level of detail. However, Section 402 of the

Congressional Budget and Impoundment Control Act excludes appropriations bills, meaning that CBO’s full account-level analysis of appropriations is only provided to selected groups such as the Appropriations and Budget Committees of each chamber.

Thus, legislators who are not on those committees and members of the public are unable to know the full fiscal effect of appropriations bills, since the reported BA and the effective BA (including gimmicks) can be

hundreds of billions of dollars apart.

With regards to the TFF, it is possible that the rescission in Section 784 of the FY 2026 Agriculture bill was scored by CBO as having some amount of OT reduction. However, since the

CBO score of the bill does not go into account-level detail, and since TFF rescissions have historically been gimmicks that do not reduce OT, it is reasonable to assume that this rescission is also a gimmick that does not reduce OT.

The Senate Appropriations Committee did not disclose the reason for including the TFF CHIMP in the FY 2026 Agriculture bill. One possible explanation is that it helps to reduce the gap between the House and Senate bills. Since the House bill’s BA was

$1.6 billion lower than the Senate’s initially reported bill, adding the CHIMP makes the new Senate bill appear slightly closer to the House level.

Congressional Options

Congress should

improve transparency by requiring CBO’s full appropriations bill analysis be published on its website. Not only would this mean that CHIMPs would be visible to more than just a relative handful of members and staff, but also the budgetary effects would be easier to explain, allowing for proper debate and discission inside and outside of Congress.

In addition to improving appropriations scoring transparency, Congress should pass budgetary rules against gimmicks that use “empty” BA reductions such as the TFF rescission to offset new spending. With the gross federal debt now more than

$38 trillion, there is no excuse for gimmicks that attempt to obscure spending.

Finally, legislators should consider strengthening due process rules around

asset forfeiture. Currently, authorities can seize assets based on a low standard of evidence, pressuring innocent people into abandoning property – which is part of why the TFF has “excess” funds in the first place.