Statutory PAYGO Background[1]

The Statutory Pay-As-You-Go (PAYGO) Act of 2010 was enacted by President Barack Obama and a unified Democrat-controlled Congress with the stated purpose to “reestablish a statutory procedure to enforce a rule of budget neutrality on new revenue and direct spending legislation.”

[2]

The PAYGO Scorecards

To implement Statutory PAYGO, the Office of Management and Budget (OMB) keeps two scorecards to track the deficit impacts of newly enacted legislation.

[3]

Deficit increases are classified as “costs” and deficit reductions are “savings.”

OMB maintains five- and 10-year scorecards. To determine the amounts entered onto each year of the scorecards, the total costs and savings of the first five and 10 years of new laws are averaged over five and 10 years, respectively. This averaging method is meant to make budgetary gimmicks to game the PAYGO scorecard more difficult.

As legislation covered by Statutory PAYGO is enacted, the costs or savings are added to the scorecards to keep a running tally.

[4]

Sequestration Enforcement

If, at the end of a session of Congress, a positive balance (called a “debit”) remains on either scorecard for the fiscal year that began on October 1, the President is required to issue a sequestration order that reduces budgetary resources of certain spending programs to fully offset the debit.

Sequestration is the cancellation or reduction of budgetary resources of spending programs by the President in response to a triggering event or other requirement in law. Sequestration has been used as a budget enforcement mechanism for several laws, including the Balanced Budget and Emergency Deficit Control Act of 1985, the Budget Control Act of 2011, and the Fiscal Responsibility Act of 2023. In these laws, as with Statutory PAYGO, sequestration has not been intended as the first option to achieve the outcome of the budget reform, but instead is a backstop to prevent fiscally irresponsible outcomes that are considered less desirable than the enforcement mechanism.

Sequestration is sometimes criticized as making “across-the-board” spending cuts, but this is far from the case. Only about 235 out of 2000 budgetary accounts, totaling approximately $150 billion, are fully subject to Statutory PAYGO sequestration. That is just 2 percent of the $6.8 trillion budget.

The programs subject to a Statutory PAYGO sequestration are the same as those subject to the Budget Control Act mandatory sequester that has been implemented annually since fiscal year 2013 and extended on a bipartisan basis into FY 2032.

[5]

Programs comprising most of the federal budget are exempt from sequestration. Social Security, veterans’ programs, most means-tested welfare programs, refundable tax credit payments, and dozens of other programs are exempt by law.

[6] Discretionary spending, including defense discretionary funding, is excluded from the Statutory PAYGO sequestration.

[7] Interest payments on the national debt are also exempt.

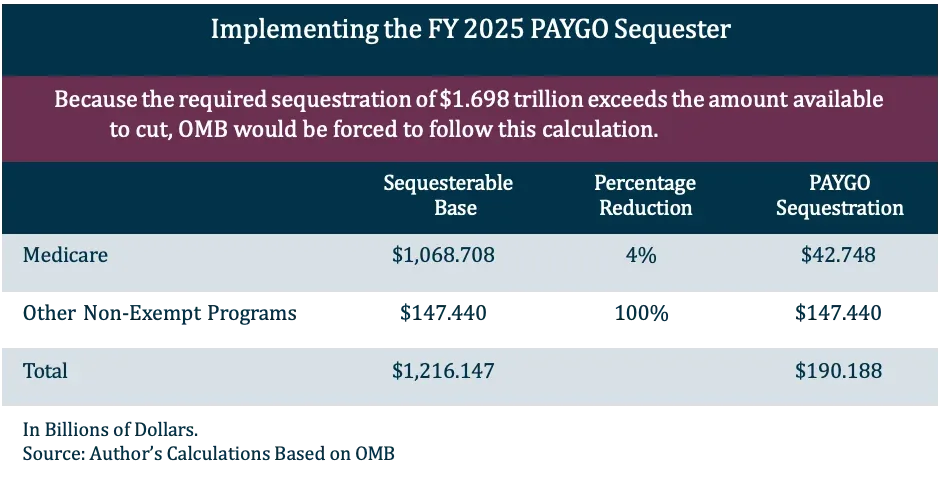

Medicare is partially subject to sequestration. Unlike other non-exempt accounts, the amount that Medicare payments can be reduced under Statutory PAYGO is capped at no more than 4 percent. According to OMB, Medicare resources subject to a Statutory PAYGO sequestration at the end of the 118th Congress would be about $1.069 trillion, so the maximum reduction in payments would be $43 billion.

[8]

According to the Congressional Research Service, “Generally, Medicare’s benefit structure remains unchanged under a mandatory sequestration order and beneficiaries see few direct impacts.”

[9]

The Current Statutory PAYGO Situation

The five-year PAYGO Scorecard has a balance of $1.698 trillion for FY 2025, while the 10-year scorecard has a balance of $914 billion.

[10] If the 118th Congress adjourns with these balances still on the scorecards, a sequestration order equal to $1.698 trillion would be required since the five-year scorecard holds the larger balance.

However, the required sequestration amount vastly exceeds the spending of accounts subject to sequestration. Therefore, the President and OMB would be required to carry out the sequestration to the fullest extent possible.

Medicare payments would be reduced by 4 percent, reducing outlays by $42.7 billion. The budgetary resources of the other non-exempt programs (such as IRS payments of transferred green energy tax credits, borrowing authority of the Commodity Credit Corporation, Obamacare cost sharing reduction and risk adjustment payments to insurance companies, and appropriated funds for the USCIS immigration examinations) would be eliminated entirely, reducing outlays by $147.4 billion. The spending reduction would be less than 3 percent of projected FY 2025 outlays.

Table 1

The sequestration order is required to be carried out not later than 14 days (excluding weekends and holidays) after Congress adjourns to end the Second Session of the 118th Congress. Assuming the

sine die adjournment is on January 3, 2025, the sequestration order must be issued no later than January 24, 2025.

The Large Balance on the PAYGO Scorecard Is from Biden’s Reckless Spending

The entire balance on the current Statutory PAYGO scorecards is due to the reckless spending that has occurred under President Joe Biden.

The FY 2023 omnibus appropriations bill transferred the PAYGO scorecard balances for FY 2023 and FY 2024 to the FY 2025 scorecard.

[11] The balance from FY 2022 had previously been transferred to the 2023 scorecard.

[12] This pushed the consequences of Biden’s spending to the end of his fourth year in office.

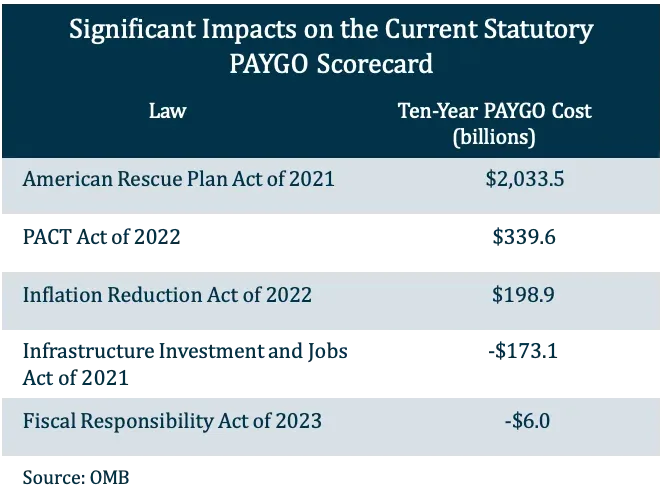

The balance on the Statutory PAYGO scorecard is primarily due to the American Rescue Plan Act (ARPA) of 2021, which had a ten-year cost of more than $2 trillion. Almost all of the costs of ARPA were within the five-year budget window, adding a $385 billion cost on each year of the five-year PAYGO scorecard. This annual cost for ARPA is larger than the available sequesterable base in each year. Thus, it is fair to attribute the need for a Statutory PAYGO sequester to ARPA.

The Inflation Reduction Act of 2022 and the Honoring our PACT Act of 2022 also added significant costs. The Infrastructure Investment and Jobs Act of 2021 recorded $173 billions of Statutory PAYGO savings (although the law actually significantly increased deficits), and the Fiscal Responsibility Act recorded $6 billion of Statutory PAYGO savings (although the law actually reduced projected deficits by more than $1.5 trillion).

[13]

Table 2

The Failures (and Opportunity) of Statutory PAYGO

As soon as Statutory PAYGO was enacted, Congressional Democrats set out to undercut it, beginning to exempt legislation from counting just 18 days later.

[14] Trillions in higher spending has been exempted from the scorecards. At times, Congress has even simply wiped the scorecards clean, as though the deficits never occurred.

The national debt has nearly tripled since Statutory PAYGO was signed into law, adding more than $22 trillion to the debt.

Spending has exploded during the Biden Administration. FY 2023 outlays were about $1 trillion higher than originally projected before Biden’s policies took effect.

[15] Excessive government spending has driven high inflation.

[16] The federal budget is on an unsustainable trajectory, with excessive spending increasing the risk of a debt spiral and the exhaustion of the federal government’s borrowing capacity.

[17]

Although Statutory PAYGO has never been enforced, it remains in law today. Lawmakers have an opportunity to use the inflection point of Statutory PAYGO sequestration to find agreement on policy improvements.

Policy Options

Although the American Rescue Plan Act was enacted through the reconciliation process, which bypasses a Senate filibuster, a provision to waive or otherwise turn off enforcement of Statutory PAYGO cannot be done via reconciliation. This is because such a provision would violate the Byrd Rule. This means that any legislation to modify enforcement of Statutory PAYGO must have bipartisan support.

Lawmakers have three basic options to respond to the pending enforcement of Statutory PAYGO:

- Enact targeted spending reductions at least equivalent to the amount that would be cut under sequestration. Statutory PAYGO would reduce spending by $190 billion in 2025. As an offset to turning off sequestration, Congress could enact other cuts that would add up to at least that amount over the next several years. These offsets could be applicable to accounts not subject to Statutory PAYGO, offering Congress flexibility in deciding which programs to impact. Policies could include extending the discretionary spending caps, rolling back costly executive actions, or rescinding funds from the Coronavirus State and Local Fiscal Relief Fund.

- Trade sequestration for other policy and process reforms. It may be easiest to find agreement on process and policy reforms that would make it worth it to turn off sequestration. For example, the Midnight Rules Relief Act would allow Congress to disapprove multiple regulations at a time under the Congressional Review Act, saving valuable floor time.[18] Administrative PAYGO rules could be strengthened to prevent executive actions from adding significant fiscal costs. Congress could determine other fiscally responsible policy and process reforms like these that are worth a sequestration-prevention agreement.

- Enforce the law and let sequestration happen. Congress may decide that the best option is the option already in law and allow the sequestration to be ordered on January 24, 2025.

Legislation attempting to waive sequestration enforcement or to clear the PAYGO scorecards would significantly increase government spending above what it would otherwise be under current law.

Congress should reject any efforts to simply waive PAYGO that are not paired with offsetting spending reductions or other policy reforms.

Statutory PAYGO Is Coming: An Opportunity for Responsible Reforms

The looming sequestration under Statutory PAYGO highlights the urgent need for responsible fiscal reforms to address the unsustainable trajectory of government spending.

By leveraging this inflection point, policymakers have a unique opportunity to implement targeted spending reductions and process improvements to improve long- term outcomes.